Investment bonds from security analysis chapter 6

Hello friends, in today’s, article we see the investment bond from chapter 6 of the security analysis book is The Selection of Fixed-value Investment. In this chapter, the authors give the perfect theory of The selection of investment bonds ( Fixed-value).

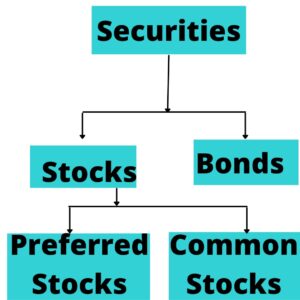

In the previous chapter, we see the classification of securities, so there are three classes of Securities. let’s recap, Class I, has the safety on principle money and has a steady income. Class II, they are divided into two types.

Type A: is have principle safety and has the conversion feature to make the possibility of profit.

Type B: In this, you can lose principle and you get lots of profits on Principles.

Class III, is about Common stocks.

so from this Part-2 of this book is begin, in this part-2 also have the five chapter so let’s start

So Part-2 is whole about the Class I securities ( fixed-value investment)

The Selection of Fixed-Value Investment: (Investment bonds)

So we talked about in the previous chapter is that we should classify securities on the basis of characters rather than on the basis of title.

In Fixed-Value type Include: (Investment bonds)

1) High-Grade straight bonds and Preferred stocks

2) High-Grade Privileged Issues.

3) Common Stocks having guarantee or Preferred status.

So It’s not fixed is that the fixed value type is only investment bonds as financial instruments.

This whole thing depends on its characteristic for they qualify for Fixed-Value Issues.

So most of the bonds are frequently associated with safety by the peoples, but they have to say like that Instead of safety is Associated with Limited return.

there was safe or not is the whole thing depends on company strength and earning power.

So let’s see what difference between bonds and preferred stocks.

- Bondholders have the first claim on companies earnings and company make them promises of payment in regular interval of time. (Investment bonds)

- So Preferred stocks also have claims but don’t have any promised with regular interest payments. So director decides to give dividends or not to the preferred stocks. there is neither priority nor Promise is assurance that of the safety of Principles.

- this depends on the company’s strength to fulfill the company obligation., so this thing is only known from the Balance sheet of companies previous year records and his execution plan and future perspective about the company.

- so from them, you know your issue is safe or not.

so the bond selection is just not like search and acceptance, it’s like a process of exclusion and rejection.

The author gives the four Principles of Selection of Fixed Value-type Securities (Investment bonds)

4 principles for selection of Fixed-Value Types Securities:

1) Safety does not depend on how many senior issues, means not by Specific lien, so lien like are the seniority of bond-like 1,2,3,4, preferred stocks and lastly common stocks.

So just like that those who hire high seniority, they have a maximum priority claim on companies asset.

The author here, try to say, ” Safety does not depend on seniority (whatever their rank) but they depend on those companies ae issue this bonds, that company have the strength to defeat their obligation.”

2) This Ability of the company to pay the interest payment. for checking this, we have to consider depression time, instead of that good time(prosperity time).

Because any mediocre company do well in prosperity time and fulfill the obligation of the company

3) If there is no safety of bonds, then given them a high coupon rate and compensation is not possible (worth it)

4) The selection of all bonds for investment purposes should be subject to rules of Exclusion and to specific quantitative tests corresponding to those prescribed by status to govern investment of saving bonds.

means the bond selection is like the government make the investment like that we have to make and our purpose is simply to make the interval of time regular income. (Investment bonds)

So in this chapter, we see only Principle 1

Principle I: Safety is not Measured by Lien, but by the ability to Pay.

So in these, there are two views on safety points.

Two views:

1) character and supposed value of the property on which bonds hold a lien,( First people think like safety

is measure by how much asset is a mortgage against that issue. so depends on seniority, so those who have the first lien against him, keep mortgage of asset means if the company is not paying their interest of first-lien seniority bond, this first lien seniority bondholder take the asset of the company under him.

so whatever is property value on that we have to buy,

So this type of people thinking on bond or senior lien

2) Strength and Soundness of obligor Enterprises ( means the safety depends on enterprises strength, so the company can pay their bills not depends on asset value.)

So in the first view, we think, they are claiming against on property.

In the Second view bond is a claim against the business. (Investment bonds)

So in this which is right,

Now you think, if the company can’t pay, then bondholders take over the companies assets and sell them and pay for themselves.

but this is not happening, so in this, there are three types of problems.

Three problems with the first view:

1 ) When businesses fail, then properties values also shrink. so companies value depends on companies earning power. If a company fails then fixed asset value also goes down.

so understanding this point the author gives the examples

Cardboard all Florida railway company, this company first mortgage is going down from 25 million to 250K dollar when the company is failing.

so the value of companies is going down when businesses fail.

the second problem is

2) You(bondholder) get the legal right with bonds, legal like You can sell the property of company, but you can’t enforce them when the company failed.

Because Court does not allow you for this.

So those are a junior lien, what they get if first lien holder sells the property and distribute themself because, the business value goes down, that why only first-lien can get money, so no money for second or third lien holder, so that’s why the court does not allow for this. (Investment bonds)

the third problem is

3) If you are allowed to take over the property by the court, so in this situation also take the lots of time and spend much money for advocate and other expense, and takes lots of delays occurred to solve the problem.

Bondholders’ motive is to avoid trouble not to found in trouble and how to goes from that troubles.

So from these principles what we learn

the first thing we learn is

Corollaries from Principle-I:

1) So there is no difference between senior or junior lien: If a company is strong then its debentures(unsecured debt) also strongs.

This debenture is a junior form of debt.

If the company strong then, their debenture also wonderful as like a first-lien bond.

So the author says, ” Strong companies debenture is better than the weak companies first lien.”

The second thing we learn is

2) Buy the highest yield: means those are a sound company or strong company, this type of company bonds, we can buy the junior bond for highest yield and you get the highest yield on that bond.

so regarding safety is all of them, not only for the first-lien bond and not for the last one lien.

This thinking present only in theory but not in practice mode, people only buy the low yield bond with the first-lien category.

The author tries to say, ” If companies junior bond is not safe then, their senior bond is also not safe so we don’t need to buy their first-lien bond.”

If a company is weak so its high-grade bond is also not safe, means if their high-grade bond is also like the low-grade bond value. (Investment bonds)

The third thing we learn is

3) If junior bonds yield and senior bond yield have the maximum difference then buy the Junior bond, If there is no difference in senior bond and junior bond, this type buy the senior bond, without taking any risk.

So buying senior bonds, they have to the protection but the yield is same, just use common sense.

What to buy in any situation, for this author give the examples

Suppose a junior lien of company X and the First mortgage bond of Company Y.

So in these two cases come forward, if we prefer the junior lien bond than the senior lien mortgage bond.

- Company X has adequate protection of total debt and the yield of junior lien bond is substantially higher than that of company Y senior lien bond.

- Buy junior lien not a senior lien, If suppose, there is not any difference between junior yield and senior yield, but the total debt protection company is more than company Y, so we can buy the junior lien.

so protection is more than those are fixed charged on bonds, which means, the Interest coverage ratio of Company X is more than the Company Y.

We can prefer the junior lien of Company X whatever not have the maximum difference between in yield.

so lastly the author says for the understanding bond. so this is the exception to the above-mentioned rules)

lastly, says the author, “Investors are not involved in this issues because they are far beyond the competence of investors and investors have to stick with this rules is the strong company has strong bonds.”

whatever we learn and use common sense to buy the junior and senior bond.

So this is all about the Investment bond from chapter 6 of security analysis.