Security Analysis Chapter 16 Book Summary

Hello friends, in today's blog, we see the Security Analysis Chapter 16 book summary, so you will able to understand the chapter with simple language. Capture Trending Market in Banknifty…

Hello friends, in today’s article, we see a summary of chapter 15 of the Security Analysis book by Benjamin Graham and David Dodd. Chapter 15 is about the Technique of Selecting Preferred Stocks for Investment. so let’s see

In this chapter, the author explains, if we decide to buy the preferred stocks while seeing their disadvantages, so author gives some techniques to select preferred stocks.

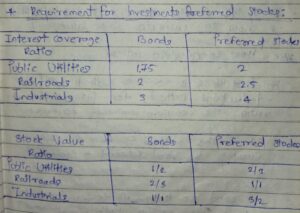

The Author Says, ” For preferred stocks, we required to stringent the minimum requirement as compared to bond. So what is the minimum requirement for interest coverage ratio, this given in the following table (image)

Now you can see, in three industry Segments

So for preferred stocks required more high multiple like in public utility is 1.75 of Fixed charges and for preferred stocks earning is 2 times of Fixed charges and Preferred stocks dividend.

Now Come for minimum stock Value requirement, in this also as compare bond and preferred stocks.

In this, you can see for preferred stocks required more. (Security Analysis: Chapter 15)

In public utilities, required 50% more than bond means 1/2 and for preferred stocks, 66.67% means 2/3 ( Bond + Preferred stocks equal)

So in this chapter 15, we discuss both tables and how to calculate this value.

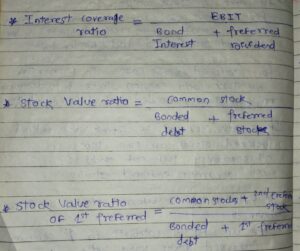

The first thing is to use the method name is ” Total Deductions method“, for interest coverage ratio to compare with minimum coverage ratio.

So in this method, we have to divide earning by Bond interest + Preferred dividend.

In Bond, we only divide by bond interest but in this, we use both ( bond interest + Preferred dividend)

so some of you say, why not we use the prior deduction method,

Because, we know that, by using the prior deduction method

the result looks like Preferred stocks are more secure than Bond. so that’s why the author uses the total deduction method.

Let’s come in Stock Value Ratios

For Bond, we use in the numerator, stocks equity( common stocks) and divided by funded debt( bonded debt).

For the preferred Stocks case, in the Numerator, We take only common stocks and in the denominator, we take bonded debt + Preferred stocks.

If Suppose You want the stock value ratio, for this preferred stocks are two type

1st Seniority preferred stocks

2nd Seniority preferred stocks

so for this type of preferred stock using the following method

In Bond, we have to take face value, and 1st preferred stocks we have to take market value.

1st preferred stocks face value we can’t take, because, preferred stocks’ actual par value is different than the stated value.

for this, the author gives example to understand the above statement

e.g, The preferred stocks and this stated par value is $1 but those are preferred stocks holders, they have to get $100 for liquidating preferred stocks.

so the actual par value of that stock is $100, not $1. so for this, we have to use Market Value.

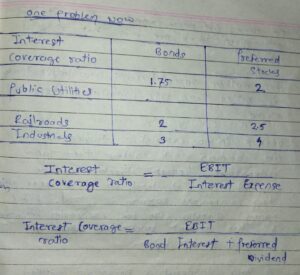

We can see tables(for referring above note page image) in that we say, for Preferred stocks the minimum requirement is more as compared to bonds.

So for seeing this formula, we know that, let’s take

The interest coverage ratio, in the numerator same ( EBIT- earning before interest tax) but in the bond case, we divided by fixed charges, and in the case of the preferred stock, we divided by fixed charges + preferred stocks dividend.

so those are preferred stock coverage is found less, because, we required maximum, as the author gives us

Let’s see in Public utility examples, for the preferred stocks the interest coverage ratio is 2 times. (as given in table by author)

Means, Interest coverage ratio = EBIT / Bond interest + preferred dividend.

Interest Coverage ratio = 2

so, for Bond ( Interest coverage ratio = EBIT / Interest charges )

Now we surprise

so its value is more than 2 times because the denominator is small

If for preferred stocks is 2, so then bond interest coverage ratio is more than 2. obviously by math

So then the author says, ” Yes, the interest coverage ratio for the bond is more than 2, but people thinks, for preferred stocks coverage ratio is have to be lenient or less stringent, (Security Analysis: Chapter 15)

Because, preferred stocks coverage ratios denominator is more, so the value may be small,”

then Author says, This type of thinking is wrong.

Because, in any company have a bond and preferred stocks, and in this company preferred stocks is when safe, then this company bond is safer, with a good margin of safety.

If the bond is less safe then how are preferred stocks safe? ( common sense)

If the coverage ratio is minimum then this is only limited to bond coverage ratio, not for preferred stocks.

that’s why the author takes 2 times the interest coverage ratio for preferred stocks and for bonds only 1.75.

then the author talks about cumulative Issues and Non Cumulative issues

Cumulative Stock issues:- Cumulative preferred stocks are those, in them, the dividend is suspended by the director, so this dividend is accumulated and this dividend is paid later.

But in Non-Cumulative Stock Issues:- In this, if the dividend is suspended, then they are not be recovered or accumulated. So those are new continued dividends, that are only given by the company.

That dividend is missed by the director, that dividend is gone forever.

Then the author says, ” Buying cumulative stocks is better than the Non-cumulative stocks.

Because, in non-cumulative stock problem is, those are common stockholder, they taking advantage, because, the director can suspend, your dividend. in those years also when companies earning is good, and this money is used by the director to improve the company. By this activity, the direct benefit to the common stockholder.

And Your dividend is missed by the company is not given in the next dividend time.

so there is not any benefit for non-cumulative stocks means full loss

On this Non-cumulative Preferred stocks lose, taking benefit by a company means on your expense, taking other profits. (Security Analysis: Chapter 15)

So those are company directors they play in trick, is that

Firstly they suspend your dividend and when they give a dividend to common stocks holder before some time that they give the dividend to the non-cumulative stockholder.

When a company wants to suspend its dividend, so for this they stop the first dividend of the common stockholder and some time after they stop the dividend of preferred stockholders also.

after this difference, the author talks about, ” those 21 preferred stocks, that do good in depression also.

Out of 440 listed stocks on NYSE in 1932, that on 21 stocks is doing good and perform well in depression with any loss.

So those are 440 listed stocks on NYSE in them only 40 (9%) are Non-cumulative preferred stocks.

By knowing this, you may be surprised, those are 21 stocks, that do good in depression, so in them,

the author gives 3 observations, they are as follows.

(snuff business is a type of business of Tobacco)

So, the author says, ” Buy seeing the only result, we can’t say, non-cumulative stocks is superior.

or we can’t have to say, preferred stocks with the bond is better than, only preferred stocks companies.

or we can’t say, Snuff business is the safe business”

Logically the author says, ” This reverse is best means, the cumulative issue is better and preferred stocks without bond is better. (Security Analysis: Chapter 15)

But this result occurs, it only proves that if this thing does not matter most and maybe desirable but you become successful or not on this things, this observation not affect.

Then the author says, In conclusion

What matters most to success.

so this is all about chapter 15 of the security Analysis book by Benjamin Graham and David Dodd.

hello friends, today, article we see the bond real estate from Security analysis book chapter 10, Specific standard for bond Investment ( continued). In this chapter, we see Criteria 6: Relation of the Value of property to the funded debt. so let’s see the bond of real estate.

As discussed soundness of bond investment depends on the oblique corporation to take the core of its depts, rather than the value of the property on which the bond has a lien.

so we say before that if a company fails, then their properties value also decreases.

so New York Statutes Recommend that the properties value is more than the 66.67% of bond issues.

let’s see an example to understand it

if Bond issued $100 million of any company, then properties value is about $167 million dollars.

so the author explains some special cases in that we have to consider the value of properties.

1 ) Equipment Trust Obligations:

These issues issued by the railroad and also called as equipment trust certificate

In this case, we kept some mortgage for this valuation so railroad companies kept the locomotive like the engine of the railway and their parts as a mortage.

this type of investment company kept and then, they issue the debt.

so in this, we have to consider the Value Because, this instrument, that companies kept as a mortgage, and they are movable and they have their sellable price ( value) because any other companies railway use this type of assets.

If company fail, then does affect on that, because we can see this to other company and get the money.

2) Collateral-Trust Obligation:-bond real estate

In this, company issue, the debt and kept as mortgage as a security purpose, that company, buy that security

means, those are investment trusts, that trust company buy the security of other company and kept their security as mortgage and issue the debt for himself.

In this companies portfolio, we know the market value of the company and we can give them loans while considering their value.

3) Real- Estate bond:

In this case, the main criteria is that how much properties value.

The company gives loans, only 66.67% of the Properties value.

so property fair value matters

so let’s see how we get the property fair value from earning power.

For this, the author gives simple examples, how do we give the loan on properties?

Example,

A home cost is about = $10,000

Rental Value is about = $1200

On the rent, you have to pay the Tax and whatever operation cost, you have to pay

so after this by paying tax and operation cost from $1200

your net income is about = $800

5% mortage, you get on that house, up to 60% of the value of properties, i.e. $6000

so 5% of $6000 = $300

so your coverage ratio is = $800 / $300 = 2.67 X

but any industrial plant they want to issue debt by they want from us

for this, we have to keep more coverage ratio, because, on that plant, this much rental value does not get us.

so after these special cases, the author gives the 7 things on Real Estate bond

1 ) Properties value increases, then rental value Increases:

If properties value decreases, then rental value also decreases

if this does not happen, then people directly buy the house instead of staying in rent, because properties value decrease but rental value increases

so Properties value increases, then rental value Increases.

2) Misleading character of Appraisals:

If sometimes, the real-Estate boom comes, then properties prices ( value) Increases.

so you have to consider those values of experienced buyers and lenders instead of the booming price of properties.

That experienced buyer wants to buy on the price, that price we have to consider instead that, we can think that if that much price is on booming time is have, then we can buy this property or not if the answer is no then don’t buy on that price.

or you can ask your friends, that price of booming time and they are comfortable to buy that price.

so let’s understand with examples

e.g. the building making cost is about $1 million and in boom time, their price increases after building full develop up to $1.5 million,

so 50% profit on making time of that building.

so let’s see a third thing or bond real-estate

3) Abnormal rental, used as a basis for Valuation:-bond real estate

let’s understand this thing, from previous examples, so property value increases 50% means, Original value is $ 1 million and in boom time is about $1.5 million

so your properties rental is abnormally high, so you have to correct them and adjust to the downside.

so in this problem is

If you get a high return i.e. 50% increase so people, try to make the building. and more and more building is developed then supply increases then all building prices suddenly goes down,

so abnormal rental, used as a basis for valuation.

4) Debt based on excessive construction cost:

in boom time, the company can issue more debt, in this boom time

because, properties construction cost is higher because, the demand for making houses is increased, so construction suppliers also increase the rate.

suppose, a cost increase of making houses is about $100 million

so now boom time, their cost is about $200 million

so you can give a loan as per the 60% rule, which is about $130 million

while properties value in boom time is $200 million but their actual price is about $100 million

so $100 million is 60% is about $60 million and you give the loan on that properties is about $130 million means your debt given that properties are not safe, and logically they did not come in 60% rule of properties.

Because, when the value of properties comes to their original fair price, then you are already paying more loan than their fair price of whole properties and loan criteria is up to 60% but you give the $130 million means more 113% of properties.

so debt is based on excessive construction costs, you have to consider this.

5) Weakness of specialized buildings:

In this people make the mistake is that the apartment house, office, storehouse, clubs, the church building

so in this people make the mistake is, they don’t differentiate between them but they have different values.

so in this, you have to treat differently because in this we can not dispose of easily while considering same value

or

this value depends on those companies they have it and they become successful, or not depends on their own value.

those are apartment buildings, they do not depend on that company, because this any can use.

for this, you have to ask for the maximum margin of safety

so for this is good that 50% margin of safety on properties on the loan amount,

in this, you have to ask for a 100% margin of safety.

so this is important is that you have to consider the weakness of specialized buildings.

6) Value-Based on initial rental misleading:

At some time, we take the initial rent for valuing properties, but those are new building their rental obviously is more

so instead of that we have to think like that while considering the new building rent instead that we have to consider after this building is old, what are the rent of this building and that rent we have to consider.

and we can approve.

because initial rent is not for the long term.

7) Lack of financial Information:

In real estate financing, the main character is, they sell the bond to the public but, they hold the stocks privately.

so companies issue, the bond, then they forgot about the bond and bondholders.

and they do not offer any financial data to the bondholder.

so this end some exception and some special case

after that author give their own suggestions

or you can see, how much you pay for buying that or any other experience buyer and lender, how much pay for that

If those are company that deals with the hotel, garage

so for this, you have to provide loan when this hotel is running well. if they are new so don’t make the deal

if they have a successful record then only give.

These are the most important things, the large loss probability in unfavorable conditions.

for this point, understanding the author gives the example

In 1933 after conditions going to improve, but those are a financial district of new york, their activity is less and that reason people gets loses and rental rate also decline so location matters most.

In this, the land has another owner and we build the building on that land.

but we pay regular payment to the landowner

so those companies build the building on that land, this land is the first mortage bond for that company.

but this is not actually the first mortage for you because first mortage of ground to the company is not for you and ground rent this company have to pay

interest coverage ratio = ground rent + interest expenses of the building increases the cost

so this is all bout the bond real estate and also chapter 10 of the security analysis book.

Hello friends, in today’s, article we see the investment bond from chapter 6 of the security analysis book is The Selection of Fixed-value Investment. In this chapter, the authors give the perfect theory of The selection of investment bonds ( Fixed-value).

In the previous chapter, we see the classification of securities, so there are three classes of Securities. let’s recap, Class I, has the safety on principle money and has a steady income. Class II, they are divided into two types.

Type A: is have principle safety and has the conversion feature to make the possibility of profit.

Type B: In this, you can lose principle and you get lots of profits on Principles.

Class III, is about Common stocks.

so from this Part-2 of this book is begin, in this part-2 also have the five chapter so let’s start

So Part-2 is whole about the Class I securities ( fixed-value investment)

So we talked about in the previous chapter is that we should classify securities on the basis of characters rather than on the basis of title.

1) High-Grade straight bonds and Preferred stocks

2) High-Grade Privileged Issues.

3) Common Stocks having guarantee or Preferred status.

So It’s not fixed is that the fixed value type is only investment bonds as financial instruments.

This whole thing depends on its characteristic for they qualify for Fixed-Value Issues.

So most of the bonds are frequently associated with safety by the peoples, but they have to say like that Instead of safety is Associated with Limited return.

there was safe or not is the whole thing depends on company strength and earning power.

So let’s see what difference between bonds and preferred stocks.

so the bond selection is just not like search and acceptance, it’s like a process of exclusion and rejection.

The author gives the four Principles of Selection of Fixed Value-type Securities (Investment bonds)

1) Safety does not depend on how many senior issues, means not by Specific lien, so lien like are the seniority of bond-like 1,2,3,4, preferred stocks and lastly common stocks.

So just like that those who hire high seniority, they have a maximum priority claim on companies asset.

The author here, try to say, ” Safety does not depend on seniority (whatever their rank) but they depend on those companies ae issue this bonds, that company have the strength to defeat their obligation.”

2) This Ability of the company to pay the interest payment. for checking this, we have to consider depression time, instead of that good time(prosperity time).

Because any mediocre company do well in prosperity time and fulfill the obligation of the company

3) If there is no safety of bonds, then given them a high coupon rate and compensation is not possible (worth it)

4) The selection of all bonds for investment purposes should be subject to rules of Exclusion and to specific quantitative tests corresponding to those prescribed by status to govern investment of saving bonds.

means the bond selection is like the government make the investment like that we have to make and our purpose is simply to make the interval of time regular income. (Investment bonds)

So in this chapter, we see only Principle 1

Principle I: Safety is not Measured by Lien, but by the ability to Pay.

So in these, there are two views on safety points.

Two views:

1) character and supposed value of the property on which bonds hold a lien,( First people think like safety

is measure by how much asset is a mortgage against that issue. so depends on seniority, so those who have the first lien against him, keep mortgage of asset means if the company is not paying their interest of first-lien seniority bond, this first lien seniority bondholder take the asset of the company under him.

so whatever is property value on that we have to buy,

So this type of people thinking on bond or senior lien

2) Strength and Soundness of obligor Enterprises ( means the safety depends on enterprises strength, so the company can pay their bills not depends on asset value.)

So in the first view, we think, they are claiming against on property.

In the Second view bond is a claim against the business. (Investment bonds)

So in this which is right,

Now you think, if the company can’t pay, then bondholders take over the companies assets and sell them and pay for themselves.

but this is not happening, so in this, there are three types of problems.

1 ) When businesses fail, then properties values also shrink. so companies value depends on companies earning power. If a company fails then fixed asset value also goes down.

so understanding this point the author gives the examples

Cardboard all Florida railway company, this company first mortgage is going down from 25 million to 250K dollar when the company is failing.

so the value of companies is going down when businesses fail.

the second problem is

2) You(bondholder) get the legal right with bonds, legal like You can sell the property of company, but you can’t enforce them when the company failed.

Because Court does not allow you for this.

So those are a junior lien, what they get if first lien holder sells the property and distribute themself because, the business value goes down, that why only first-lien can get money, so no money for second or third lien holder, so that’s why the court does not allow for this. (Investment bonds)

the third problem is

3) If you are allowed to take over the property by the court, so in this situation also take the lots of time and spend much money for advocate and other expense, and takes lots of delays occurred to solve the problem.

Bondholders’ motive is to avoid trouble not to found in trouble and how to goes from that troubles.

So from these principles what we learn

the first thing we learn is

1) So there is no difference between senior or junior lien: If a company is strong then its debentures(unsecured debt) also strongs.

This debenture is a junior form of debt.

If the company strong then, their debenture also wonderful as like a first-lien bond.

So the author says, ” Strong companies debenture is better than the weak companies first lien.”

The second thing we learn is

2) Buy the highest yield: means those are a sound company or strong company, this type of company bonds, we can buy the junior bond for highest yield and you get the highest yield on that bond.

so regarding safety is all of them, not only for the first-lien bond and not for the last one lien.

This thinking present only in theory but not in practice mode, people only buy the low yield bond with the first-lien category.

The author tries to say, ” If companies junior bond is not safe then, their senior bond is also not safe so we don’t need to buy their first-lien bond.”

If a company is weak so its high-grade bond is also not safe, means if their high-grade bond is also like the low-grade bond value. (Investment bonds)

The third thing we learn is

3) If junior bonds yield and senior bond yield have the maximum difference then buy the Junior bond, If there is no difference in senior bond and junior bond, this type buy the senior bond, without taking any risk.

So buying senior bonds, they have to the protection but the yield is same, just use common sense.

What to buy in any situation, for this author give the examples

Suppose a junior lien of company X and the First mortgage bond of Company Y.

So in these two cases come forward, if we prefer the junior lien bond than the senior lien mortgage bond.

so protection is more than those are fixed charged on bonds, which means, the Interest coverage ratio of Company X is more than the Company Y.

We can prefer the junior lien of Company X whatever not have the maximum difference between in yield.

so lastly the author says for the understanding bond. so this is the exception to the above-mentioned rules)

lastly, says the author, “Investors are not involved in this issues because they are far beyond the competence of investors and investors have to stick with this rules is the strong company has strong bonds.”

whatever we learn and use common sense to buy the junior and senior bond.

So this is all about the Investment bond from chapter 6 of security analysis.