Security Analysis: Chapter 15

Hello friends, in today’s article, we see a summary of chapter 15 of the Security Analysis book by Benjamin Graham and David Dodd. Chapter 15 is about the Technique of Selecting Preferred Stocks for Investment. so let’s see

The technique of Selecting Preferred Stocks for Investment:-Security Analysis: Chapter 15

In this chapter, the author explains, if we decide to buy the preferred stocks while seeing their disadvantages, so author gives some techniques to select preferred stocks.

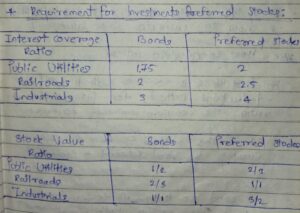

The Author Says, ” For preferred stocks, we required to stringent the minimum requirement as compared to bond. So what is the minimum requirement for interest coverage ratio, this given in the following table (image)

Now you can see, in three industry Segments

So for preferred stocks required more high multiple like in public utility is 1.75 of Fixed charges and for preferred stocks earning is 2 times of Fixed charges and Preferred stocks dividend.

Now Come for minimum stock Value requirement, in this also as compare bond and preferred stocks.

In this, you can see for preferred stocks required more. (Security Analysis: Chapter 15)

In public utilities, required 50% more than bond means 1/2 and for preferred stocks, 66.67% means 2/3 ( Bond + Preferred stocks equal)

So in this chapter 15, we discuss both tables and how to calculate this value.

How to calculate Rations?

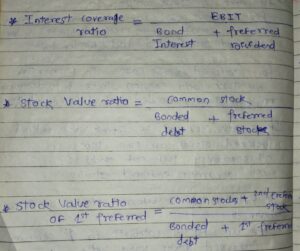

The first thing is to use the method name is ” Total Deductions method“, for interest coverage ratio to compare with minimum coverage ratio.

So in this method, we have to divide earning by Bond interest + Preferred dividend.

In Bond, we only divide by bond interest but in this, we use both ( bond interest + Preferred dividend)

so some of you say, why not we use the prior deduction method,

Because, we know that, by using the prior deduction method

the result looks like Preferred stocks are more secure than Bond. so that’s why the author uses the total deduction method.

Let’s come in Stock Value Ratios

For Bond, we use in the numerator, stocks equity( common stocks) and divided by funded debt( bonded debt).

For the preferred Stocks case, in the Numerator, We take only common stocks and in the denominator, we take bonded debt + Preferred stocks.

If Suppose You want the stock value ratio, for this preferred stocks are two type

1st Seniority preferred stocks

2nd Seniority preferred stocks

so for this type of preferred stock using the following method

- If we want to calculate for 1st seniority preferred stocks Value ratio. so In 1st seniority of preferred stocks in the Nenomenator of equation presents 2nd seniority preferred stocks + common stocks and in the denominator, we can use Bonded debt + 1st preferred stocks. (Security Analysis: Chapter 15)

In Bond, we have to take face value, and 1st preferred stocks we have to take market value.

1st preferred stocks face value we can’t take, because, preferred stocks’ actual par value is different than the stated value.

for this, the author gives example to understand the above statement

e.g, The preferred stocks and this stated par value is $1 but those are preferred stocks holders, they have to get $100 for liquidating preferred stocks.

so the actual par value of that stock is $100, not $1. so for this, we have to use Market Value.

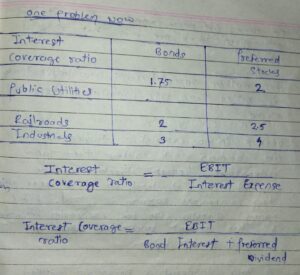

We can see tables(for referring above note page image) in that we say, for Preferred stocks the minimum requirement is more as compared to bonds.

So for seeing this formula, we know that, let’s take

The interest coverage ratio, in the numerator same ( EBIT- earning before interest tax) but in the bond case, we divided by fixed charges, and in the case of the preferred stock, we divided by fixed charges + preferred stocks dividend.

so those are preferred stock coverage is found less, because, we required maximum, as the author gives us

Let’s see in Public utility examples, for the preferred stocks the interest coverage ratio is 2 times. (as given in table by author)

Means, Interest coverage ratio = EBIT / Bond interest + preferred dividend.

Interest Coverage ratio = 2

so, for Bond ( Interest coverage ratio = EBIT / Interest charges )

Now we surprise

so its value is more than 2 times because the denominator is small

If for preferred stocks is 2, so then bond interest coverage ratio is more than 2. obviously by math

So then the author says, ” Yes, the interest coverage ratio for the bond is more than 2, but people thinks, for preferred stocks coverage ratio is have to be lenient or less stringent, (Security Analysis: Chapter 15)

Because, preferred stocks coverage ratios denominator is more, so the value may be small,”

then Author says, This type of thinking is wrong.

Because, in any company have a bond and preferred stocks, and in this company preferred stocks is when safe, then this company bond is safer, with a good margin of safety.

If the bond is less safe then how are preferred stocks safe? ( common sense)

If the coverage ratio is minimum then this is only limited to bond coverage ratio, not for preferred stocks.

that’s why the author takes 2 times the interest coverage ratio for preferred stocks and for bonds only 1.75.

then the author talks about cumulative Issues and Non Cumulative issues

Non-cumulative stocks Issues/ cumulative Stock issues:-

Cumulative Stock issues:- Cumulative preferred stocks are those, in them, the dividend is suspended by the director, so this dividend is accumulated and this dividend is paid later.

But in Non-Cumulative Stock Issues:- In this, if the dividend is suspended, then they are not be recovered or accumulated. So those are new continued dividends, that are only given by the company.

That dividend is missed by the director, that dividend is gone forever.

Then the author says, ” Buying cumulative stocks is better than the Non-cumulative stocks.

Because, in non-cumulative stock problem is, those are common stockholder, they taking advantage, because, the director can suspend, your dividend. in those years also when companies earning is good, and this money is used by the director to improve the company. By this activity, the direct benefit to the common stockholder.

And Your dividend is missed by the company is not given in the next dividend time.

so there is not any benefit for non-cumulative stocks means full loss

On this Non-cumulative Preferred stocks lose, taking benefit by a company means on your expense, taking other profits. (Security Analysis: Chapter 15)

So those are company directors they play in trick, is that

Firstly they suspend your dividend and when they give a dividend to common stocks holder before some time that they give the dividend to the non-cumulative stockholder.

When a company wants to suspend its dividend, so for this they stop the first dividend of the common stockholder and some time after they stop the dividend of preferred stockholders also.

after this difference, the author talks about, ” those 21 preferred stocks, that do good in depression also.

Out of 440 listed stocks on NYSE in 1932, that on 21 stocks is doing good and perform well in depression with any loss.

So those are 440 listed stocks on NYSE in them only 40 (9%) are Non-cumulative preferred stocks.

By knowing this, you may be surprised, those are 21 stocks, that do good in depression, so in them,

the author gives 3 observations, they are as follows.

- The number of Non-cumulative issues was higher than cumulative issues, in those 21.

- No. of preferred stocks proceeded by bonds were higher than without bonds in those 21. ( as we discussed, in those company, that have only preferred stocks, that’s is good for the preferred stockholder.)

- The industry best represented is the snuff business, with three companies.”

(snuff business is a type of business of Tobacco)

So, the author says, ” Buy seeing the only result, we can’t say, non-cumulative stocks is superior.

or we can’t have to say, preferred stocks with the bond is better than, only preferred stocks companies.

or we can’t say, Snuff business is the safe business”

Logically the author says, ” This reverse is best means, the cumulative issue is better and preferred stocks without bond is better. (Security Analysis: Chapter 15)

But this result occurs, it only proves that if this thing does not matter most and maybe desirable but you become successful or not on this things, this observation not affect.

Then the author says, In conclusion

What matters most to success.

- Outstanding record of the company for a long period in past

- The strong inherent stability of the company

- Absence of concrete reason to expect substantial change for worse in the future.

so this is all about chapter 15 of the security Analysis book by Benjamin Graham and David Dodd.