Financial Literacy to become rich

Hello friends, I am Laxman Sonale, In today’s article we see the financial literacy to become rich from chapter 11:- ‘why must one invest’ from the book ” Stock To riches ” by Parag Parikh. In this chapter, you know the difference between rich people and poor and middle-class people’s income, their expenses. The most important how we become rich.

so let’s start

Chapter 11:- Why must one Invest:-Financial Literacy

In the starting, the author gives a quote on today’s situation.

“Modern man drives a mortgaged car over a bond financial highway on credit card gas.”

– Early Willson

In this chapter, the author talks about the basics of financial literacy. let’s see what he say

the author says, ” I would like to end the book with some thoughts on the paradigm of money and the basic of financial literacy. these concepts are very well explained in the Rich dad, poor dad series authored by Robert T. Kiyosaki with Sharon L. Lechter.

We are afraid of losing money, of not having enough to make. if you have a passion for anything you will accept by passion helps you to think positively. But when you do that you will never have enough money to fulfill your desires.

People believe that money can solve all their problems, but that idea is an illusion.

Remember when you were just out of college. you had certain desires to be fulfilled and certain bills to be paid. so you were thrilled when you got a job. (Financial Literacy)

you believed that the paycheque at the end of the month would solve all your problems when the paycheque arrived you paid the bills for your desires. you were happy about it, but this happiness was short-lived.

As soon as you fulfilled your desires, they increased and you required more money to fulfill your desires. they increased and you required more money to fulfill those new desires.

When you got a hike in your salary the pleasure was again short-lived for your desires increased in proportion to your income.

It’s a never-ending story and you are always afraid that you will never have enough. so every time you think of money fears grips you and you make decisions not with your mind but with your heart.

What you need to do is to change your paradigm. passion should drive you not to fear, think of what you can do with money and what you should do to make it.

money is an idea. you see it more clearly with your mind than your eyes. learning to play the game of money is an important step on your journey to financial freedom.”

after this explanation, then the author talks about learning the money game.

Learning the Money Game:- Financial Literacy

in this point, the author shows how money works for rich people, middle-class people, and poor people.

the author says, ‘ To be a successful investor you must know how money works, there are some elementary facts about finance that unfortunately are not taught in schools and colleges. (Financial Literacy)

so let’s begin, learning now

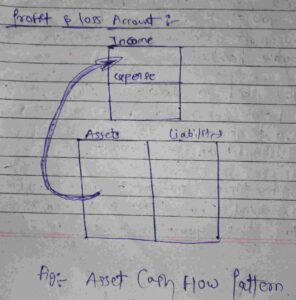

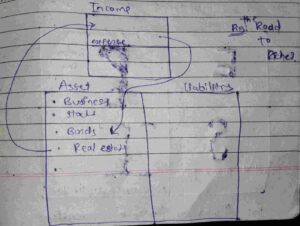

The question you should ask Yourself: What is an Asset?

Answer:- An asset is that which creates an income for the owner.

see the following image to understand better.

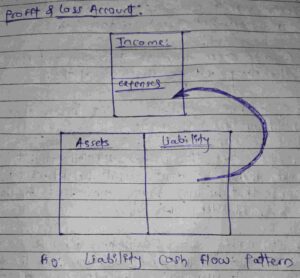

Question: What is Liability?

Answer:- A liability is that which creates an expense for the owner.

see the following image to understand better.

then the author gives the difference between asset and liability with bank examples

author says,” have you been approached by banks willing to lend you money to buy a house? Does your banker say he will help you buy an asset?

Attractive deals in the form of low-interest rates and long-term mortgage payments are offered. so you go ahead and buy your dream house thinking you are buying an asset.

By the definition of an asset, it should create an income for you. however, here it is creating on expense in the form of mortgages, taxes, interest, etc.

so common sense demands that you treat it as a liability rather than an asset.”

then, the author explains, why a banker tells you, a house is an asset.

the author says, ” Yes, the banker did tell you that you are buying an asset. what he did not tell you was that he was buying the asset for the bank and a liability for you.

There is nothing wrong in buying a house and mortgage, but understand that you are thereby creating a liability for yourself that will entail further expenses. even if you buy a house with your own money and kept it locked you should treat os as a liability as you are incurring expenses for its upkeep in the form of maintenance charges, property tax, society charges. etc. (Financial Literacy)

However, if you buy a house on mortgage and rent it, and your rental income is higher than the mortgage, then you have a positive cash flow.

House becomes an asset as it generates an income. Understanding how assets and liabilities work is basic to Financial Literacy.

Your cash flow is an indication of whether you are building assets or taking liabilities. if income is coming in your pocket, you have an asset, if income is going out of pocket, it is a liability.

Once you understand this you can work out your own financial future.”

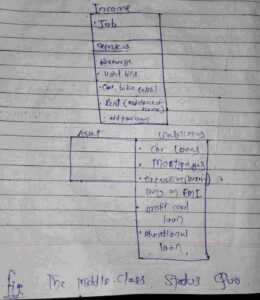

then the author explains the Cash Flow of middle-class

Cash flow of the Middle-Class People:

In this, the author says, ” A majority of the customers of bank and consumer goods companies come from the middle-class. it is not because of their inherent purchasing power but because they happen to be attractive borrowers.

They are cautious about money yet, as they strive to improve their standard of living they get increasingly into debt. all their lives they work to pay off their mortgages, credit cards bills, car longs, etc.

they start small, like taking a loan to buy a two-wheeler, but soon their desires increase and they want to buy a car. so they go to the bank and take a car loan to fulfill their desire. with a bigger loan, the outgoings increase and they desperately look for a hike in their salary.

the hike comes and with it the desire to buy a bigger car. so the bank offers them a bigger loan. and this goes on and on. expense move and an increase in salary are soon nullified.

Only the liability increase; no-effect is a mode to increase the asset. they don’t realize that they have started working for the bank also ( by taking up liabilities.)

Now they work for two bosses. One who provides the job, and the bank to whom they give the interest, mortgage, etc?

this is the cash flow of the middle-class, which you will understand better from the following image.

As the income of the middle-class increase so does their liabilities.

they make little effects to create assets Instant gratification and financial illiteracy dominate their decision-making. they believe, they are creating assets in the form of houses, cars,s, etc. whereas they are only creating liabilities and increasing their expense. (Financial Literacy)

see the following image to understand middle-class people status quo

What differentiates the middle class from the rich is their lack of financial literacy.

it is the cash flow that makes all the difference the rich understand the power of money and they make it work for them. they always have a positive cash flow.”

then the author talks about the cash flow of the rich.

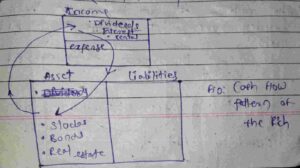

Cash flow of rich people:-

in this the author says, ” the rich create assets, the assets create income, from they create more assets. even if they buy a house on mortgage, they rent it and the rentals are higher than the mortgage and other charges they pay.

so the house is an asset for them even if they take a bank loan to acquire it. see the following image to understand better way.

the balance sheet of the rich consists of assets like stocks, bonds, real estate, etc.

their income derives mainly from dividends, interest, rental, etc. they make their money work for them and they do not create liabilities.

thus their expenses are under control. anyone can do what the rich do.

Firstly it requires discipline to stay the course and avoid instant gratification of desires.

Secondly, it requires an understanding of the basic principles of assets and liabilities. it’s easy to become financially literate if you have the patience.

some say that money begets money these people should have stayed rich, they lost only because they were not financially literate.

they did not know, how to harness the power of money. To become rich you must have a passion for money. Making money is a game and you must enjoy playing it. It is tough but worth the trouble.”

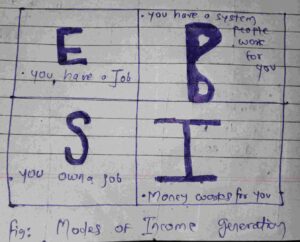

then the author gives fours ways of making money.

the author says, ” there are four ways by which people make money ad each method forms one quadrant of the income generation circle. (Financial Literacy)

different people fall into different cash quadrants depending upon the source of their cash flow.

- Employee cash flow quadrant:- they work for somebody and earn a salary as employees.

- Self-employed cash flow quadrant:- they are the professionals like, doctors, lawyers, architects who are self-employed.

- Businessman cash flow quadrant:- they are the ones who own a business.

- Investor cash flow quadrant:- they are investors whose income comes from investments.

to which quadrants do you belong.

whichever quadrant you may be, if you want to make your money work for you need to make every effort to get into the investor quadrant.

Only then will you be able to achieve financial freedom.

A lot of us would love to be in the business quadrant, but few of us are not blessed with the skills or the abilities, or the resources to run a business.

so the best alternative would be to take a share of the profits of the company by way of dividends and capital appreciation. to gain a detailed perspective on the above concepts I would strongly recommend to the read the rich had, poor dad, cash flow quadrant by Robert T. Kiyosaki with Sharon L. Lechter ( C.P.A.)”

then the author talks about the best form of investment,

for that, you can read this in the book,

buy the book from the following image link

So this is all about the chapter 11 summary of the book ” stocks to riches ” by Parag Parikh on Financial literacy.