Security Analysis Chapter 16 Book Summary

Hello friends, in today's blog, we see the Security Analysis Chapter 16 book summary, so you will able to understand the chapter with simple language. Capture Trending Market in Banknifty…

Hello friends, in today’s article, we see a summary of chapter 15 of the Security Analysis book by Benjamin Graham and David Dodd. Chapter 15 is about the Technique of Selecting Preferred Stocks for Investment. so let’s see

In this chapter, the author explains, if we decide to buy the preferred stocks while seeing their disadvantages, so author gives some techniques to select preferred stocks.

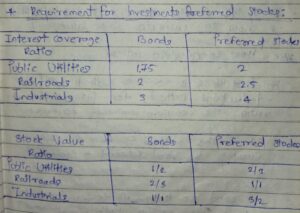

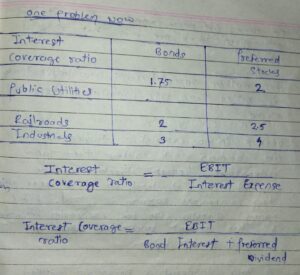

The Author Says, ” For preferred stocks, we required to stringent the minimum requirement as compared to bond. So what is the minimum requirement for interest coverage ratio, this given in the following table (image)

Now you can see, in three industry Segments

So for preferred stocks required more high multiple like in public utility is 1.75 of Fixed charges and for preferred stocks earning is 2 times of Fixed charges and Preferred stocks dividend.

Now Come for minimum stock Value requirement, in this also as compare bond and preferred stocks.

In this, you can see for preferred stocks required more. (Security Analysis: Chapter 15)

In public utilities, required 50% more than bond means 1/2 and for preferred stocks, 66.67% means 2/3 ( Bond + Preferred stocks equal)

So in this chapter 15, we discuss both tables and how to calculate this value.

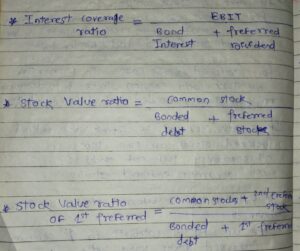

The first thing is to use the method name is ” Total Deductions method“, for interest coverage ratio to compare with minimum coverage ratio.

So in this method, we have to divide earning by Bond interest + Preferred dividend.

In Bond, we only divide by bond interest but in this, we use both ( bond interest + Preferred dividend)

so some of you say, why not we use the prior deduction method,

Because, we know that, by using the prior deduction method

the result looks like Preferred stocks are more secure than Bond. so that’s why the author uses the total deduction method.

Let’s come in Stock Value Ratios

For Bond, we use in the numerator, stocks equity( common stocks) and divided by funded debt( bonded debt).

For the preferred Stocks case, in the Numerator, We take only common stocks and in the denominator, we take bonded debt + Preferred stocks.

If Suppose You want the stock value ratio, for this preferred stocks are two type

1st Seniority preferred stocks

2nd Seniority preferred stocks

so for this type of preferred stock using the following method

In Bond, we have to take face value, and 1st preferred stocks we have to take market value.

1st preferred stocks face value we can’t take, because, preferred stocks’ actual par value is different than the stated value.

for this, the author gives example to understand the above statement

e.g, The preferred stocks and this stated par value is $1 but those are preferred stocks holders, they have to get $100 for liquidating preferred stocks.

so the actual par value of that stock is $100, not $1. so for this, we have to use Market Value.

We can see tables(for referring above note page image) in that we say, for Preferred stocks the minimum requirement is more as compared to bonds.

So for seeing this formula, we know that, let’s take

The interest coverage ratio, in the numerator same ( EBIT- earning before interest tax) but in the bond case, we divided by fixed charges, and in the case of the preferred stock, we divided by fixed charges + preferred stocks dividend.

so those are preferred stock coverage is found less, because, we required maximum, as the author gives us

Let’s see in Public utility examples, for the preferred stocks the interest coverage ratio is 2 times. (as given in table by author)

Means, Interest coverage ratio = EBIT / Bond interest + preferred dividend.

Interest Coverage ratio = 2

so, for Bond ( Interest coverage ratio = EBIT / Interest charges )

Now we surprise

so its value is more than 2 times because the denominator is small

If for preferred stocks is 2, so then bond interest coverage ratio is more than 2. obviously by math

So then the author says, ” Yes, the interest coverage ratio for the bond is more than 2, but people thinks, for preferred stocks coverage ratio is have to be lenient or less stringent, (Security Analysis: Chapter 15)

Because, preferred stocks coverage ratios denominator is more, so the value may be small,”

then Author says, This type of thinking is wrong.

Because, in any company have a bond and preferred stocks, and in this company preferred stocks is when safe, then this company bond is safer, with a good margin of safety.

If the bond is less safe then how are preferred stocks safe? ( common sense)

If the coverage ratio is minimum then this is only limited to bond coverage ratio, not for preferred stocks.

that’s why the author takes 2 times the interest coverage ratio for preferred stocks and for bonds only 1.75.

then the author talks about cumulative Issues and Non Cumulative issues

Cumulative Stock issues:- Cumulative preferred stocks are those, in them, the dividend is suspended by the director, so this dividend is accumulated and this dividend is paid later.

But in Non-Cumulative Stock Issues:- In this, if the dividend is suspended, then they are not be recovered or accumulated. So those are new continued dividends, that are only given by the company.

That dividend is missed by the director, that dividend is gone forever.

Then the author says, ” Buying cumulative stocks is better than the Non-cumulative stocks.

Because, in non-cumulative stock problem is, those are common stockholder, they taking advantage, because, the director can suspend, your dividend. in those years also when companies earning is good, and this money is used by the director to improve the company. By this activity, the direct benefit to the common stockholder.

And Your dividend is missed by the company is not given in the next dividend time.

so there is not any benefit for non-cumulative stocks means full loss

On this Non-cumulative Preferred stocks lose, taking benefit by a company means on your expense, taking other profits. (Security Analysis: Chapter 15)

So those are company directors they play in trick, is that

Firstly they suspend your dividend and when they give a dividend to common stocks holder before some time that they give the dividend to the non-cumulative stockholder.

When a company wants to suspend its dividend, so for this they stop the first dividend of the common stockholder and some time after they stop the dividend of preferred stockholders also.

after this difference, the author talks about, ” those 21 preferred stocks, that do good in depression also.

Out of 440 listed stocks on NYSE in 1932, that on 21 stocks is doing good and perform well in depression with any loss.

So those are 440 listed stocks on NYSE in them only 40 (9%) are Non-cumulative preferred stocks.

By knowing this, you may be surprised, those are 21 stocks, that do good in depression, so in them,

the author gives 3 observations, they are as follows.

(snuff business is a type of business of Tobacco)

So, the author says, ” Buy seeing the only result, we can’t say, non-cumulative stocks is superior.

or we can’t have to say, preferred stocks with the bond is better than, only preferred stocks companies.

or we can’t say, Snuff business is the safe business”

Logically the author says, ” This reverse is best means, the cumulative issue is better and preferred stocks without bond is better. (Security Analysis: Chapter 15)

But this result occurs, it only proves that if this thing does not matter most and maybe desirable but you become successful or not on this things, this observation not affect.

Then the author says, In conclusion

What matters most to success.

so this is all about chapter 15 of the security Analysis book by Benjamin Graham and David Dodd.

Hello friends, in this article, we see the chapter 14 summary of the book Security Analysis. Chapter 14 is all about the What is Preferred stocks, and their origin story, and also their advantage and disadvantage.

So, from this chapter, we discuss the only preferred stocks, and their Analysis based on the Advantages and Disadvantages of the Investor to buy that preferred stocks. let’s start

The author told, In The Intelligent Book also is that Preferred stocks are not Attractive Investment, it is Unattractive Investment.

The author says, ” Preferred stocks represent an Unattractive form of investment.”

so let’s find out why

Because 1st reason is that the Preferred stocks Principle and their income return is limited. whatever they told first is that amount only paid by the company.

and Second Reason the author told, is that Those are Preferred stocks holder, they don’t have any Claim on company. or in the author’s words is that ” Interest payment gets at any cost.”

and also Author says, ” Preferred stocks are the Limitations of Bond and Stocks Mixers, and Preferred stocks are more vulnerable than bond at the worst Condition of company.” (Security Analysis Chapter 14)

Because preferred stocks have a claim after Bond Holder.

Ans:

The difference is that those are bond interest is compulsory to pay by the company, if the company is not paying, this type of company called a Defaulter.

Those are preferred stocks Dividend payment depends on the Board of directors of the Company, they pay or not pay.

If a company’s earnings are good and also make more than the preferred stock’s dividend, so usually preferred stock payment is done, but in this claiming point of preferred stocks looks unusefulness ( no benefited ).

If Companies Perform Bad and they generate very low earning, so bondholders have a claim on the Asset of the company, but they don’t have Practical value of that asset just like, we discussed in the bond Analysis series in all previous chapters. (Security Analysis Chapter 14)

Because, If the business fails, then properties value also fail, means decreases

so Investor think and they make the general rule, ” Bond instruments form is not have the special advantage as compare to preferred stocks. If the company is good then preferred stocks and bonds are also good. If the company is bad, then the bond is also bad.”

Read this again and think above two lines.

But the author says, ” this type of investor thinking is not good. Preferred stocks are weaker than Bonds.”

Because, bondholders get the money but those are directors of the company, they stop preferred stocks dividends.

why this happen

Because, if the company is capable, but they don’t pay preferred stocks dividend, and they give a reason like, that the Company has the good time in future, for that purpose they suspend the dividends of the preferred stocks. and say if the company grows, then you get the benefit also. for example, like, the company wants to expand.

that’s why they try to collect cash and save cash or in future any emergencies come, for that emergencies, they save the cash to deal with that problem. (Security Analysis Chapter 14)

so this happens with preferred stocks dividends.

so those are preferred stocks holder have the following types of conflict problem

1 ) first is that what happens in the company I don’t care, I just want the continuous income.

2) Second is, If Company suspends the dividend, in the future, the company will perform well and become a great company.

and If the company uses the proper money of the holder of the preferred stock, then they get a good return on that money in the future.

so these two types of conflict of interest come to preferred stocks holder, and also a conflict of interest come between preferred stocks holder and commons stocks holder

Because, if companies director stops payment of preferred stocks dividend, then this money helps to build a company or grow the company.

so Because of this activity, common stocks holder get more benefits than the holder of the preferred stock

how this when, let’s see

When a company grows, then earing grows and share price is also growing so that’s benefit goes to the Common Stocks holder.

Preferred Stocks holders, not get the benefit of the company growth, because they get regular, whatever the dividend payment. This payment depends on what decides when we buy that preferred stocks.

So being great company, they don’t get benefit or advantage of that great company, as much as we see one side.

On the Other Side, The common Stocks Holder gets a benefit on earning and the preferred stockholder gets a benefit on companies expenses.

And also Board of Director of companies have also the conflict of Interest

Many times, they favor Common stocks holder, more than preferred stockholders, because they give the vote for the selection of companies’ board of directors. (Security Analysis Chapter 14)

Or In many times, the board of directors is not favored for common stocks holders, instead of that, they favor Management people.

Because, they get the salary, from the management. so many times, they don’t see the best interest of the common stockholder or preferred stocks holder, instead of that, they only see their own best interest.

Then the author says, ” this is the weakness of preferred stocks holder as compared to the bondholder.”

there is only one solution is that Preferred stocks holder has to be voting rights on the enterprise when the dividend is suspended by the director, then preferred stocks holder have to be immediately voting control to put money in the right place.

But practically is not happening. If in any company happen like this then preferred stockholder not take good advantage of that voting right.

So this thing of control also becomes useless.

Then after this author says, ” Yield or risk is not Commensurable.”

High Yield is not offset High risk

If you buy preferred stocks, and you have fear is that you will lose your principal amount and for this offer company give you a high dividend yield. so for this, they don’t offset.

What thing is offset is the thing is you have to get a good chance of principle profits, without losing it.

let’s see some qualifications of preferred stocks

Here is one question come is that what criteria to buy preferred stocks

The author says, ” there are Three criteria for buying preferred stocks.”

1) Preferred stocks, have to fulfill the Minimum requirement of bonds

2) Exceed these minimum requirements by a margin to offset discretionary Feature of Dividend payment ( means those bonds minimum requirements, they have to exceed well with good margin)

Because we have those risks ( which risk) is the board of directors of the company can suspend our dividend payment, because, they have the power for this.

then author show, the 21 companies list, in those company have preferred stocks that were listed on New York Stock Exchange in 1932.

Between 21 companies only 5 companies perform well in depression also.

then, the author says, ” Sound Preferred stocks are not impossible things, but it is exceptional phenomena.”

exceptional because sound preferred stocks are the mistakes of the company. (Security Analysis Chapter 14)

Why mistake,

The mistake is, because, the company can issue bonds but they issue preferred stocks.

If they issued the bond, they get the Tax benefit, but on preferred stocks, they don’t get that benefit.

If preferred stocks perform well, then the company don’t get benefit from them, because the preferred stockholder is only benefited.

and on dividend company have to pay tax.

The author says, ” Issuing preferred stocks only benefits the company, because, they can stop any time dividend of preferred stocks.”

If the company is not suspending the dividend of preferred stocks, then the benefit is going to the holder of the preferred stock, because, company issues bonds but they issue preferred stocks and they don’t get tax benefits also.

Now some Investor says, Like that, We don’t agree with this, because the company is giving limited income to the preferred stocks and the company can invest properly money, that comes from by issuing preferred stocks and can get the better return on their investment ( that money come from by issuing preferred stocks). Whatever company pay to preferred stockholder on that basis company earn double profit. so this benefit gets the company.

But, the author tries to say is that ” the main purpose of preferred stocks is that company can suspend dividend at any time.”

So in this case, then the author is right.

Because in this case the only company is benefited

If the dividend suspends the loss goes to the preferred stockholder and if the dividend payments, then the company gets lost. (Security Analysis Chapter 14)

So if this type of Problem happen in preferred stocks, then why this is very much popular ( in 1940 before)

then the author says, ” just before the first world war, the majority preferred stocks is the industrial issues and they have speculative natures.”

Because they get discounted price than the par value. so profit possibility is moe and after that continue for 15 years got prosperity in the USA in 1920 on this basis preferred stocks give the awesome return.

On this basis, preferred stocks perform better than bonds, but actually, that is not.

Then the author talks about the study of the University of Michigan.

The University recently study ( 1940) and then, the author observes and prove that

Preferred stocks are without bond is better than preferred stocks with bond.

This means, If a company issue bond and preferred stocks and you buy preferred stocks of this company so this is not a wonderful idea, instead of that you can buy the preferred stocks of those company that don’t issue bonds.

When adverse development happens means depression/ recession comes, then company earnings decrease, so in that, if the company has issued the bond, then this bond gets benefited, than preferred stocks. so buy only those companies’ preferred stocks, they are not issued the bonds.

The other thing, the author observe from the Michigan university’s study is that preferred stocks stability depends on common stocks stability.

If common stocks decline then preferred stocks also decline.

then Author says,” is like, if Head’s come win common stocks, and if tail comes, preferred stocks lose.”

Why do common stocks holder win?

Because Heads means the good performance of the company and common stocks holder get unlimited capital gain.

And tail means, Company perform badly then preferred stocks also decline in values, as same as common stocks holder.

If Investor Analysis is good and they think in the future company give a multi-bagger return, then why do you buy preferred stocks instead that buying common stocks and participating in profit.

If the Investor is doubtful then buy the preferred stocks, why this doing is good

because they have to take risk of principle by buying Common stocks.

so they get lost, so they don’t have to do, at that point they get the good opportunity to principle profit.

so this is all about Chapter 14 of the Security Analysis book by Benjamin Graham and David Dodd.

Hello friends in today’s article, we see chapter 12 of the Security analysis book. In this chapter, we see a special factor in the Analysis of Railroad and Public-Utility companies. so let’s start with Railroad Bond analysis.

so let’s, in this

The authors said, ” those are railroad companies they have maximum data. so those are individuals who have the competency to analyze data correctly.

The author also, says, ” if we have to do high-grade bond analysis, then why we invest in this bond, instead of a bond.

we can invest in stocks, with that much analysis, which means, there are no more benefits of analysis when we invest in the high-grade bond.

Just we have to keep remember is that those are income generating, they are more above the interest charges means good interest coverage ratios. (Security Analysis: Chapter 12)

so another thing, is that those are stock value ratio is also high.

Then the author talks about the railroad industry general things like

those are light traffic, they go in the truck, and those are passenger traffic they go in their own car.

so only heavy traffic remains for Railroad, traffic like, Coal, iron steal, mineral transport.

so railroad success, depends on this thing also, that much increases then profit increases.

and another also quantitative part is an available book, if you want to learn, more about the railroad, then buy the book from the following link

so let’s start with Public Utility company bond analysis

In public utility bond analysis have three problems, they are as follows

1 ) People think, the application of the term of the public utility to on industrial operations.

so this is not the right thing, for the right things, we have to define and understand the public utility definition.

Public utilities are those types of companies that are providing essential services under government regulation and the most important thing is on public utility is ‘ they are stable and have legal right to charge that much to be a profitable and good return on capital investment.

stability means,

They are relatively stable with other companies in the same industry.

then the author says,” Nowadays, pseudo Utility comes more like, selling ice, operating taxi cabs, owning cold storage plant. so people also called, then also public utility.

So this is the first problem,

so these are actually industrial operations but they mean people called them a public utility.

Nowadays their combination come( 1933)(author talk in 1933, don’t forget that)

like, Natural gas is combined with Ice Plant. (Security Analysis: Chapter 12)

2) the second problem is that this one bond issue whatever their prospective they use the prior-deductions method to calculate interest coverage ratio.

we lastly talk about this method, is they are a useless method, we have to use total method.

This problem is that those are junior bond issues, they are more covered properly as compare to senior bond issues.

If you apply common sense, you see these are nonsense things.

3) the third problem is that companies do not include the depression charges, while considered or finding interest coverage ratio. if they may be understated depression or not include then.

If someone says, your depreciation is the only bookkeeping thing concept, then your money is not spent properly.

then it means, that if you listen then or agree with them, that means they make you fools or you become a fool by them.

Depression is important and you have to subtract them, because, your instruments use daily, and their value becomes less sometimes later they become obsolete.

So that instruments losing their power by using daily, for that we have to subtract depreciation and other problem is unstable in this problem, the author says,

minimum 10% of gross revenue and 4% of total profit value, that much have to subtract.

If you want to be more conservative, then you can take 12% of gross revenue as a minimum.

4) there is the fourth problem is that

those are Federal taxes are imposed after deduction interest.

How you can find, = EBIT/interest expenses

But most of the time, those are corporate people, in their reports, they deduct the tax first, and then show the earning, and then coverage ratio is found. (Security Analysis: Chapter 12)

So you don’t give the tax paid first, so in this, you don’t worry about from where I am and add tax and earning the become minimum.

So this is a good thing, you have become more conservative and you take past then actual earning, so this is no problem.

because they don’t give any big difference by adding tax.

But if you analysis of a Holding company bond, then, you have to worry about some

So those are holding company they have to pay subsidiaries and their subsidiaries bond issues and preferred stocks payments.

So holding company, first have to pay their subsidiaries preferred stocks or bond issues, and after that holding companies bond issues charges.

so in this, we have to consider the tax.

Those are preferred dividends, you have to pay to subsidiaries and tax on them and after whatever earnings come, you can use it. (Security Analysis: Chapter 12)

Then the author gives the Example, How a company fools the Investor.

The companies debenture Issues, they have price is about $3,000,000

and companies business is, this company operate 20 telephone companies and 4 ice companies.

Value of property = $12,500,000

After depreciation, this value is equal to $1650 per $1000 bond issues after deduction of prior obligations.

so following are the income account.

Gross earnings – $3,361,000

Net Before Depreciation – $969,000

Prior Deductions – $441,000

Balance for Debentures – $528,000

interest on Debentures – $195,000

Balance for Stocks – $ 333,000

the Balace is above 2.71 X(times) interest on this issues.

so how they found this,

so Coverage ratio= Debentures balance / Interest of debentures

coverage ratio = $528,000 / $195,000

coverage ratio = 2.71X

the question arises

What is the problem with these ratios

so the first problem in this is as follows

1) Business combined means, the actual utility is mixed with industrial operations but they are ice plants. (Security Analysis: Chapter 12)

and they don’t give the gross and net income of ice plants

we don’t know how much percentage from the ice plant and how much percent from the telephone company.

so they don’t give us

if we assume ice business give maximum percentage income, that’s why they try to hide this.

second problem

2) the second problem is Depreciation is not subtracted.

Those are other telephone companies whose 15% of gross revenue is the depreciation.

so,

If we take 15% of depreciation = 15% of $3,361,000

depreciation = $ 500,000

If we take Net income after depreciation = $969,000 – $500,000

Net Income = $ 469,000

and then we take calculations as follows, we get the result

Balance for debentures = $ 469,000 – $441,000

Balnce for debentures = $ 28,000

and Interest on debentures = $ 195,000

so they are not equal to the debentures

this is the trick

so if we can not assume $500,000 depreciation, Because, those are ICE plants, their depreciation is very less.

so we can assume depreciation as $300,000 ( i.e. 9th 1/2 % of Gross revenue.)

third problem

3) Third Problem is that they used the prior- Deductions method.

In this we get the debentures safety

Debentures safety = $ 528,000 / $195,000

Debenture safety= 2.71X

and If we see for the senior bond issue, we get as follows

Senior bond safety= $969,000 / $441,000

Means Senior Issue is less secured and Debenture issues is more secure(junior bond issues)

So this is not a logical thing, as compared to the seniority (Security Analysis: Chapter 12)

If we make the right income account is as follows

Restating property:

Gross Earnings – $3,361,000

Net before Depreciation – $969,000

Depreciation – $ 300,000

Balance for Interest – $669,000

Total Interest Charges – $441,000 + $195,000

Total Interest charges – $636,000

Coverage Ratio – $669,000 / $636,000

Coverage Ratio – 1.05X

so forth problem

4) So fourth problem is that,

they say, $1650 of property value behind each $1000 debentures

so given,

Property Value – $12.5 million

Total Debt – $ 10.5 Million

Senior debt – $7.5 Million

Debentures – $ 3 million

so how much actual coverage ratio, we get

let’s find it out

for that,

Calculations:

property Value / Total Debt = $ 12.5 M / $10.5 M = 1.19

( M denote here – Millions)

It means only, i.e. $1190 of property value behind $1000 of total Debt.

so what companies say, How they get see following calculations

where they misguided ( mistake) (Security Analysis: Chapter 12)

Property Value for Debentures = $ 12.5 M – $ 7.5 M

Property Value for debentures:- $ 5 M

Debentures = $ 3 M

Property / total Debt = $ 5 M / $ 3 M

so that why come $ 1650

so in this time, they used the prior deductions method ( that method secure junior) to fool investor

if we apply for senior, then they are $ 1400 of property value behind each $1000 of senior debt.

Means Senior is less safe if we see the only a number

so this type, Companies make fool to investor

hello friends, today, article we see the bond real estate from Security analysis book chapter 10, Specific standard for bond Investment ( continued). In this chapter, we see Criteria 6: Relation of the Value of property to the funded debt. so let’s see the bond of real estate.

As discussed soundness of bond investment depends on the oblique corporation to take the core of its depts, rather than the value of the property on which the bond has a lien.

so we say before that if a company fails, then their properties value also decreases.

so New York Statutes Recommend that the properties value is more than the 66.67% of bond issues.

let’s see an example to understand it

if Bond issued $100 million of any company, then properties value is about $167 million dollars.

so the author explains some special cases in that we have to consider the value of properties.

1 ) Equipment Trust Obligations:

These issues issued by the railroad and also called as equipment trust certificate

In this case, we kept some mortgage for this valuation so railroad companies kept the locomotive like the engine of the railway and their parts as a mortage.

this type of investment company kept and then, they issue the debt.

so in this, we have to consider the Value Because, this instrument, that companies kept as a mortgage, and they are movable and they have their sellable price ( value) because any other companies railway use this type of assets.

If company fail, then does affect on that, because we can see this to other company and get the money.

2) Collateral-Trust Obligation:-bond real estate

In this, company issue, the debt and kept as mortgage as a security purpose, that company, buy that security

means, those are investment trusts, that trust company buy the security of other company and kept their security as mortgage and issue the debt for himself.

In this companies portfolio, we know the market value of the company and we can give them loans while considering their value.

3) Real- Estate bond:

In this case, the main criteria is that how much properties value.

The company gives loans, only 66.67% of the Properties value.

so property fair value matters

so let’s see how we get the property fair value from earning power.

For this, the author gives simple examples, how do we give the loan on properties?

Example,

A home cost is about = $10,000

Rental Value is about = $1200

On the rent, you have to pay the Tax and whatever operation cost, you have to pay

so after this by paying tax and operation cost from $1200

your net income is about = $800

5% mortage, you get on that house, up to 60% of the value of properties, i.e. $6000

so 5% of $6000 = $300

so your coverage ratio is = $800 / $300 = 2.67 X

but any industrial plant they want to issue debt by they want from us

for this, we have to keep more coverage ratio, because, on that plant, this much rental value does not get us.

so after these special cases, the author gives the 7 things on Real Estate bond

1 ) Properties value increases, then rental value Increases:

If properties value decreases, then rental value also decreases

if this does not happen, then people directly buy the house instead of staying in rent, because properties value decrease but rental value increases

so Properties value increases, then rental value Increases.

2) Misleading character of Appraisals:

If sometimes, the real-Estate boom comes, then properties prices ( value) Increases.

so you have to consider those values of experienced buyers and lenders instead of the booming price of properties.

That experienced buyer wants to buy on the price, that price we have to consider instead that, we can think that if that much price is on booming time is have, then we can buy this property or not if the answer is no then don’t buy on that price.

or you can ask your friends, that price of booming time and they are comfortable to buy that price.

so let’s understand with examples

e.g. the building making cost is about $1 million and in boom time, their price increases after building full develop up to $1.5 million,

so 50% profit on making time of that building.

so let’s see a third thing or bond real-estate

3) Abnormal rental, used as a basis for Valuation:-bond real estate

let’s understand this thing, from previous examples, so property value increases 50% means, Original value is $ 1 million and in boom time is about $1.5 million

so your properties rental is abnormally high, so you have to correct them and adjust to the downside.

so in this problem is

If you get a high return i.e. 50% increase so people, try to make the building. and more and more building is developed then supply increases then all building prices suddenly goes down,

so abnormal rental, used as a basis for valuation.

4) Debt based on excessive construction cost:

in boom time, the company can issue more debt, in this boom time

because, properties construction cost is higher because, the demand for making houses is increased, so construction suppliers also increase the rate.

suppose, a cost increase of making houses is about $100 million

so now boom time, their cost is about $200 million

so you can give a loan as per the 60% rule, which is about $130 million

while properties value in boom time is $200 million but their actual price is about $100 million

so $100 million is 60% is about $60 million and you give the loan on that properties is about $130 million means your debt given that properties are not safe, and logically they did not come in 60% rule of properties.

Because, when the value of properties comes to their original fair price, then you are already paying more loan than their fair price of whole properties and loan criteria is up to 60% but you give the $130 million means more 113% of properties.

so debt is based on excessive construction costs, you have to consider this.

5) Weakness of specialized buildings:

In this people make the mistake is that the apartment house, office, storehouse, clubs, the church building

so in this people make the mistake is, they don’t differentiate between them but they have different values.

so in this, you have to treat differently because in this we can not dispose of easily while considering same value

or

this value depends on those companies they have it and they become successful, or not depends on their own value.

those are apartment buildings, they do not depend on that company, because this any can use.

for this, you have to ask for the maximum margin of safety

so for this is good that 50% margin of safety on properties on the loan amount,

in this, you have to ask for a 100% margin of safety.

so this is important is that you have to consider the weakness of specialized buildings.

6) Value-Based on initial rental misleading:

At some time, we take the initial rent for valuing properties, but those are new building their rental obviously is more

so instead of that we have to think like that while considering the new building rent instead that we have to consider after this building is old, what are the rent of this building and that rent we have to consider.

and we can approve.

because initial rent is not for the long term.

7) Lack of financial Information:

In real estate financing, the main character is, they sell the bond to the public but, they hold the stocks privately.

so companies issue, the bond, then they forgot about the bond and bondholders.

and they do not offer any financial data to the bondholder.

so this end some exception and some special case

after that author give their own suggestions

or you can see, how much you pay for buying that or any other experience buyer and lender, how much pay for that

If those are company that deals with the hotel, garage

so for this, you have to provide loan when this hotel is running well. if they are new so don’t make the deal

if they have a successful record then only give.

These are the most important things, the large loss probability in unfavorable conditions.

for this point, understanding the author gives the example

In 1933 after conditions going to improve, but those are a financial district of new york, their activity is less and that reason people gets loses and rental rate also decline so location matters most.

In this, the land has another owner and we build the building on that land.

but we pay regular payment to the landowner

so those companies build the building on that land, this land is the first mortage bond for that company.

but this is not actually the first mortage for you because first mortage of ground to the company is not for you and ground rent this company have to pay

interest coverage ratio = ground rent + interest expenses of the building increases the cost

so this is all bout the bond real estate and also chapter 10 of the security analysis book.

Hello friends, in today’s article we see Investment Grade Corporate Bonds and their specific standard for bond investment ( criteria 3, 4 & 5) from chapter 9 of the Security Analysis book. so let’s see one by one criterion

In this chapter we see the three types of criteria and what told by the New York statute and Benjamin Graham what advice us. so let’s start with this

In these provision means, what are the Characteristics of Bonds, and what condition that affect the interest rate and what happens effect of maturity on bond character and their price.

so those things come in bond Indenture that come also inn this means provision of issues

and What is the seniority of bond, and what are their mortgage debenture, so this all comes in the provision of issues.

Those are the New York Statute, that we talk earlier,

so they only allow mortgage secure bonds from public utility groups and not allowed debentures.

so debentures are allowed only for railways but not a public utility.

On this point, the author says, ” Unsecured bond issues of any groups without any reason, reject them is not right, whatever the lien on the company, so nothing happen.”

The debenture is also one type of liens like unsecured debt, and junior lien, and above this, the mortgage bond is also present. (Investment Grade Corporate Bonds)

then the author says, ” those are investors they are more attachment with maturity debt. so those are short maturity”

they are safer Because your maturity comes near, and those are long maturity people they are a risky bond investment.

but the author says, ” this type of thinking is very wrong”

Because, of that, so those are short maturity, they have to refinance and the company needs good cash to repay for those are short maturity that comes as an obligation to the company.

or if they have strong financial and good earning power, then they can issue new bonds and raise the fund.

so some companies do issue short maturity because they don’t have a good credit rating to issue long-term maturity bonds. (Investment Grade Corporate Bonds)

so this type of company, most of the time gets the trouble for investors.

then author discusses some examples in that author takes the short and long issue of the same bond.

For Examples.

In 1932,

the Bond is First 5s, this bond short maturity in 1934 and long term maturity in 1944.

so in this bond, only maturity difference occurs all rating and coupon rates are the same.

First 5s means, they are first in seniority of bonds, and 5s means 5% coupon rate, if 5s instead that 6s means 6% coupon rate.

Debenture means, they are unsecured

So Due to 1934 means, maturity in 1934

Due to 1944 means, maturity in 1944

I hope basic terminology you understand

let’s come with examples

so those short bonds which mature in 1934, their price is $96.5, and those 1944 long term mature bond price is $35.

means those are mature in 1934, they, you can buy on $96.5 and those are mature in 1944 their price, so you can buy is $35. (Investment Grade Corporate Bonds)

so what happened in 1934, the company pay off the short-term maturity bonds by the company.

so those issue of 1944, their price increases up to $91.

so this long-term bond ( 1944) is a good opportunity because in this principle profit we get.

the author gives another example

Secured 6.5s, and their maturity in 1933 and secured 6.5s, their maturity for the long term in 1935.

The price of the short-maturity bond is $94 and

Long maturity bond price is $43

so this both issues, company payoff at maturity

so in this also long term issue is a good opportunity to investment

because you get the cheap price of a long-term maturity bond.

Other issues

In 1938 First 5s bond, price is $99.88 and they mature in 1944

First 5s bond, for long term maturity in 1954 bond price is $45

so both are default in 1939, before his maturity. (Investment Grade Corporate Bonds)

those are price is $99.88 decrease to $36

and the price of long term maturity bonds decreases to $20

so those are very expensive and short term maturity bonds, their price is highly falling than long term maturity bonds.

so like this author gives the two and three examples

the author also says, ” Is this is not meaning to buy maturity bond that is cheap and long term bond, just because they are cheap.”

so seeing Safety is important, if safety standards, we have to satisfy, if the company does not satisfy with the safety standard, then we don’t have to buy that bond, because we are not benefiting and taking the risk of losing principal.

this is all come in criteria 3

so let’s see criteria 4

so start with as per the New York Statutes

So after this new york statute rules, then the author says, ” suppose there are new municipalities establish, then according to them then, don’t get the finance, and they can’t wait for 25 years, so those are new states, they can’t wait for 10 years if they follow the rules of New York statutes. means, they don’t get finance.”

So those default in 10 years or 25 years, then they don’t get the finance if we follow the new york statutes.

Then for this, The author says, ” This is the different stringent rule, so what is a solution or so for this, buy the high coupon rate bond, then you have the risk of principal loss. (Investment Grade Corporate Bonds)

So the author says, “this is not a good idea just like before say so many times”

so right way is the author says, ” you have to stringent your own standard because those happen failure in 25 years of companies part to compensate with them your stringent standard.”

Like see this thing,

the city or state what if they rehabilitate, their and reduce the expenditure and increases the Tax rate to collect maximum revenue and also minimize the debt and reorganization of corporate in companies.

so this thing you have to see to invest in their bonds,

So then you ask for a higher yield is not because you have a loss of principle instead that to satisfy yourself.

So before is bad, and I take high yield, so this listening looks, weird.

but the author says, that

so let’s talk about dividend Record

Dividend record is company pay the dividend record before 5 years, in past.

so the myth is that those are companies that pay the dividend, they are strong companies

so this looks logically good, because if the company has money, then only they pay the dividend.

So the company has money and they issue a bond, and bond investment is also good.

so then the author says, ” company pays the dividend regularly, then we only know that companies financial strength is good, but those are bondholder,

they don’t have any direct benefit instead that they got the loss because, companies resources are used by the common stockholder, and companies cash is payable to the stockholder,

so in future, some difficulties come, then companies don’t have the cash to pay for bondholders.

so this thing, you can know from companies balance sheet that company is sound, so that necessary to pay a dividend, so they have money to pay dividend bu they not paying, so this thing is better than paying a dividend.

so in dividend-paying companies have this advantage is, if company cancel the dividend, then we know companies in the future have some difficulties so that line company concern the dividend because, their problem in future performance. (Investment Grade Corporate Bonds)

But, in this have difficulty is if some company perform bad and condition is weak bu they pay the dividend because, their credit rating is going low so this is very dangerous things, we have to stay attentive on that.

so summary of dividend criteria is those companies pay the dividend, they have some condition, we have to see that condition, and what benefited to the bondholder, then only you have to invest in that companies bond.

so let’s talk about criteria 5

This is also, interest coverage ratio, and this is also interest earing multiple)

to this is important, so this called as Margin of safety.

So what say New York Statutes

Railroad ( Mortage bonds):

on this, the New York Statute says, 1.5X of earning interest charges in past 6 years out 5 individuals year.

so means, In the past 6 years, in 5 years the interest coverage ratio is 1.5X

or

The recent year is important and there are the first year and remaining 5 years in that any 4 years.

so those are debentures or income bonds of railroads. (Investment Grade Corporate Bonds)

(on income bond we can talk later when we talk about the preferred stock)

so in this multiple is 2X in the latest year ( previous first year) and in past 5 years in that 4 years of any four years.

Those are Public utilities:- their earning is 2X in past 5 years average of interest charges

so we talk about in railroads of individuals year of past years,

but in public utility, we take an average of years.

So get the value of interest coverage ratio, you have to know about three things

so for this author give the three things that help you to consider interest coverage ratio, so let’s see

so let’s see the Method of computation of interest coverage ratio: in this author give three methods that people used in previous past time, and also suggest which is best

a) Prior deduction method

b) Commutative deduction method

c) Total deductions method aka. Overall methods

so all methods discussed while taking examples

a) Prior deduction Method

Suppose A company, $10 million worth of First Mortage 5% bond, and Debentures worth $5 million.

and companies average earning is $1,400,000

so the company have to pay interest on the first mortgage is 5% of $10 million is equal to $500,000

so coverage ratio is = $1,400,000/$500,000 = 2.8X

and remain is = $1,400,000 – $500,000 = $900,000

so those are junior debentures for this they have to pay 6% on $ 5 million of debenture

so interest on 6% = $300,000

so coverage ratio = $900,000 / $300,000 = 3X

The stupid thing is

those are senior bonds their coverage ratio is 2.8X and those are junior bonds and their coverage ratio is 3X

it means that junior issue is more protected than senior issues. (Investment Grade Corporate Bonds)

So these things are very stupid,

Because obviously those are senior bonds they have more protection than the junior bond and they got first money when the company is failing. but in that not happen like that so

this method is a useless method and misleading method, but so many companies use this ratio in past and they fool the investor and investors also do stupid things and don’t think about this and they only see quantitative but not see qualitative.

So people forgot the figure and people go in calculation and say, this value is original whatever they come.

They forget also, whatever value comes, they are not checked for is sensible or not.

b) Commutative Deduction method:

In these, those are the first mortgage, and they are the same as above mentioned

because, on that method, no one is superior

so the ratio is for the First 5s = 2.8X is coverage ratio ( calculate above)

so come for a debenture,

for debenture, in this method, First of all, you have to pay first mortgages

so $800,000 , total interest charges

so debenture 6% ratio = $1,400,000/ $500,000 + $300,000 =1.75X

so this method is good, than the first method, because, it looks sensible

but the author says, ” we have to use the third method i.e. Over all method or total reduction method.”

This means whatever, you buy ( senior or junior) total debt safety is required.

so for both ( first and debenture 6s also)

for this, you have to add junior and senior interest charged i.e. $500,000 + $300,000

then ratio is = $1,400,000/ 800,000 = 1.75X

for both

because, if junior lien default, then, his effect also happens on senior in coming future.

If you buy senior issues ( mortgage bonds), they can also use this method

Add junior and senior interest charge for ratio

if you consider your own interest expense then you get more than good things and have added in advantage

but don’t use that rule. (Investment Grade Corporate Bonds)

so for total, this rule and added advantages

now let’s talk about other points

2) Amount of coverage required:

in this author give the specif coverage ratio for each and every category

so this ratio author gives from his experience and their practices and also see companies history in depression also.

3) Period Required for Test:

So New York Statutes says, you have to take a period of five years and also says, for utility take an average of five years and for railroads take an independent year of 4 in past and immediate precious year not in taht.

so for this author says, 7 years period is better than 5 years period

and we can also modify it by increasing or decreasing year by seeing previous year performance

Suppose, we invest in 1940, in that time you can take 7 years, but year 1933 is in depression so for this, you can take only 6 years, by modifying according to the situation and that is very helpful.

If you invest in 1934 or 1935, so in this time, you can’t help with 7 years period, because in that 3 years in the depression, so for this you have to take 10 or 12 years of the time period to unusual things is average out the depression time freme. (Investment Grade Corporate Bonds)

so in this, you have two kind situation

in the first situation, you can take the actual earning in depression(whatever come -ve) year for interest coverage ratio, but interest coverage ratio is come very less, so for this author says, ” take the Zero earning of those years that are in a depression instead that taking whatever is coming.

and consider time period for 12 years and take their average and after that found the ratio ( coverage ratio)

so this author recommends, instead of separate,

the author says, after this all, we have to see other points also

” We have to see what are the average trends and minimum figure and also the current figure.”

so suppose earning profit increases means, a rising trend is going, then this is good and current showing figure is also good, then better and you get the good margin on that then also better in a rising trend.

If earning Trend is Unfavorable ( downward trend,) then you don’t have to accept until the first thing is the earning ratio is required maximum.

The second thing is the earning trend is downward, then you have to confirm that this trend is temporary ( instead is not only I think so it’s not like this reason) you have to good conviction reason why goes high this trend.

so these are all things we have to conclude while investing in bonds.

hello friends, in today’s, article, we see the specific standard for bond investment from chapter 8 of the security analysis book and also what is a bond, how we invest in them, and what are the problems come while investing in bonds.

In principle 4, we talk about those states, they have their own laws and rules on those that are saving banks that can invest in specific areas.

or

they have to satisfy their criteria of states

So the author (Benjamin graham and David dodd’s) use the New York Status, because, he thinks it’s a good point to start.

After that, whatever its criteria, the author criticism them and if need to neglect them or reject them also and they modified them if required.

So there are 7 criteria prescribed by New York Statutes:

In the Coming 4 chapters we explain the 7 criteria in this, we see only two criteria.

So firstly the author explains, what the new york statute says, and what author explains his own view if they are right or wrong

1 ) New York Statute says, ” You can invest in U.S. government bond, state bonds, municipal bond”

but You can not invest in foreign government and foreign corporation bonds.

2) You can invest in Railroad, gas, and telephone industry, b

but you can not invest in street railway and water companies and also in debentures of public utilities.

3) You can invest in the first mortgage on a real estate bond,

but you can not invest in all industrial bonds and also financial companies’ bonds, investment trust, and credit concern companies also.

so for this author give some problems with New York statutes

1 ) In any industry, we can’t invest, so this is not talking about practically way because, in the industry also, there are some companies that perform well in bad times also and we can select them.

If we neglect whole industry segment then, what remain only railroads and public utility and government bond according to the New York Statutes.

So it’s happening, if we can’t find good then don’t go for bad.

so this is like we are doing narrow and it’s not right, so we can include the industrial also.

2) Water companies neglect the public utility by the New York Statutes and don’t give a good reason and other states include the water company and we also include them.

3) In 1938, One commitment that happens in the banking sector is in that they do the consortium of banks can waive as many rules as it sees fit, and they decide which criteria can remain and eliminate and also do modifications according to them by doing a simple variation.

so for this, the author says, ” Until now there is not any problem of consortium bank, but happen problem in future.”

so we don’t have to take tension because, nowadays, no consortium bank, that told us to do this or that.

4) Foreign government restriction is a good restriction according to the author, because, the foreign government pays or does not pay. If they don’t pay you, so you can’t force them to pay and you can’t take their asset, and revenue source,

the author gives examples of some countries that full fill the obligation and some more countries that don’t fulfill the obligations.

like those fulfill obligation country are Canada, Holland, and Switzerland, etc.

after that, the author talks about foreign company bond investment.

So many cases, present there, those fulfill the obligation by a foreign company but not that time government doesn’t fulfill it.

but sometimes the company is able to pay but the government restricts them.

So sometimes exchange is restricted on the company by the government.

so the foreign company has the ability to pay but they can’t pay, because the government does not allow it.

The author says those are a small company that is very much vulnerable at unexpected changes.

so those are big companies, they can go easily and unexpected harsh condition goes easily. means, they can pass easily in dangerous situations also.

Because, they have good relation with bank and they have lots of resources, that deals with that situation.

so New York statute, what say, about this criterion is

In railroad, in that much amount of mine is spread over the area, and in municipal bonds, that much amount of population is required and in public utility, they say different types of criteria, but in this point that much is not important, if you want to know about them then, buy a book by clicking above image of book.

So come here directly and what author reconnects

The author says, ” buy municipality bonds when the population is 10 thousand or by public utility when gross revenue is about $2 million and on the railroad, the gross revenue is $3 million

and lastly, in the industrial, the gross revenue is $5 million.

Industrial is not included in New York statute, because they don’t say, to b buy or avoid them

and author says, ” invest in industrial also.”

So large size does not mean to have safety

so it’s may happen those are the largest companies that are the weakest company.

if they have maximum debt.

So large size criteria are not affected in this municipality, railroad, and public utility,

so small and large both are the same.

but in industrial, have an effect, those are large size, they are more stable than small size.

So this is all about the two criteria for specific standards for bond investment.

Hello friends, in today’s, article, we see how to invest in bonds, from chapter 7 of Security analysis. while investing in bonds, you can consider some principles of that, in we see the two principles( second and third) of investing in bonds, from chapter 7 of security analysis.

so let’s see one by one steps of investing in bonds.

Previous Chapter 6 on Investment bonds

This explains the two principles of investing in bonds.

so let’s see one by one

In Good conditions, every bond performs the great, but when depression comes, then we know which bond is strong or weak.

So in depression, the bond will be safe or not

on these two views come forwards

so you have a question What is the means of Character of the industry?

it means, Company comes in those industries, that industry has some immunity in depression condition.

for example, Light companies, Water supply companies, the telephone company. (How to invest in bonds)

and another question, What are the means of Amount of Protection?

it means, having a good Margin of Safety

means, Margin of Safety is high as much as that can not affect depression also.

In bond Context, the Margin of Safety is the Interest Coverage ratio ( times interest earned, Earning multiples)

so in this chapter whenever word comes coverage ratio, that means earning multiple, interest coverage ratio.

The Amount of Protection required those companies like steel companies, Automobiles, etc.

You need a maximum amount of protection because they fluctuate more.

So The author ay,s ” Those companies are good companies that perform well in depression also.”

The author says, ” Character of Industry is more important than the Amount of Protection because those companies perform good in depression, then minimum safety is considered as good.

Because In depression Maximum safety is also eroded.

So the author also, says, ” Not any industry is resistance to the depression, so the quest on is how much difference occurs in that industry’s company.”

That much percentage of the company is stable in depression as compared to competitors, then we can get maximum protection also. (How to invest in bonds)

This means the Minimum coverage ratio is sufficient for us

So if Maximum unstable company, then that much amount of earning multiple then, we ask for a good margin of safety.

If in some companies the Instability is more then, don’t buy this companies bond, whatever the maximum coverage ratio.

so Coverage ratio calculated formulae are

Coverage ratio = Earning before interest Tax / Interest expense ( interest charges)

Suppose a company pays $1 interest on a bond, and company earnings are $10 so then the coverage ratio is 10.

or Earning multiple 10.

Means, How much multiple companies generate the earning on an interest basis. so the company does a maximum coverage ratio then the company is safe and they give the regular payment of bonds.

The character of Industry reflects the difference in stability and required coverage ratio.

so the author says, there are three types of company, we can classify

These are different, because, these companies have different stability

1 ) Public utility is stable, and the railroad is less stable than public utility and Industrials is very less stable than Railroads.

So in these three types, we required different coverage ratios, that much minimum required to buy that company, so that’s why they are different. (How to invest in bonds)

So Public Utilityis more stable, so for this less Coverage ratio is sufficient

The railroad is only stable, then they required more coverage ratio, than a public utility.

Industrial companies required a maximum coverage ratio than railroad companies because they are unstable.

Then, The author talks about industries, why bonds collapse in depression

so which companies bond collapse in depression,

so let’s talk about public utility.

the author observed that the large size companies, that do a good deal in depression time, then small companies so small and mediocre companies do very bad in depression.

so in big companies in their problem is, large-size companies present very little. and their debt outstanding is not more because they retire the bond issues.

So is that not means, if you don’t get the good company, then buy bad companies bonds.

Public says, ” those are secondary companies, how they get capital, if you only buy large companies bonds and finance them, so this activity affect the small and mid-size companies.”

so for this, the author says, ” We don’t take their responsibility and save them while sacrificing our capital, so in this type of securities not take in this type of securities not come in Class I of Fixed-value type investment.

If they want funds from us, then they have to give us a good chance of making profits on principal money, if we have principle loss risk.

So on bond financing, people view as following

that’s both are generally accepted views of people.

so from this, we get the message is only weak companies have to issue the bond.

so for this message, the author says, ” If only a weak company issues the bond, then we don’t have to buy that bond.”

then the author told, their view on Bond Financing

so let’s understand with examples, (How to invest in bonds)

Suppose loan is 2, 3% and you make the 20 and 30%, then you can easily ready to take a loan, so just like that of the company also.

the company gets the bond for 4,5% and they make 50 or 60% profits.

After that, the author talks about unsound practices that are followed in the industry.

1 ) Railroad company issues bonds because their earning is poor and then stock, sales fluctuate, then the author says,” don’t buy this type of Bonds.

2) Some strong companies, issue bonds to pay the debt. so during this activity management problem is solved, but shareholders’ problems increases and their dilution starts, and companies free from debt.

So from this principle 2

we learn two things

so let’s talk about principles 3

means, if some companies bonds, have risk to lose principle, but company give you high coupon rate and give you high yield but you can lose principal money.

so buying this type of bond is not good.

Because there is no relation between yield and risk.

Because, that the risk of loss is indefinite and no one is predicting and you can’t says, while seeing that past to handle risk. (How to invest in bonds)

Just like Life insurance, fire insurance in that you can see the previous data and people’s mortality rate and doing actual computation and from that, we can say, about the relation of risk and yeild.

but in this we can’t says about risk and yeild relation.

because in this the loss is not defined uniformly they are concentrated at particular intervals, like depression everyone gets lost.

And the author says, ” while accepting principle lose, instead of high coupon rate just like become an insurance company.

In an insurance company, you pay the premium and if you have lost like, fire in the house some life-death, so then you get the payment from another side.

you can say like principles because you pay the premium on that.

so if lose events happen then only you get the money.

So in this situation, you become the insurance company and the company pays you a premium on a risky bond, and they take your principle money first, and then they give you a premium on each 6 month interval time.

and if you have lost, then forgot the principles money.

so the author says, ” this is not a good idea, because those are individual then, can’t distribute money like an insurance company. if they distribute like an insurance company but when college, they lose everything in depression. (How to invest in bonds)

so that’ why not good idea

then the author says, ” If you have to take the principle to lose risk, then you can’t offset by the high coupon rate instead of that, offset of risk, you have to get a good chance on that principles to get good profits.

For example, ‘ if you buy bond then buy very much at a discount of par value.

so in this, you have profits possibility and also have lost possibility.

both have a chance or instead that but the conversion bond that converts in stocks, in future.

For example, if you invest $100, and you can lose $100, so in this situation, you have to be possible is that $100 becomes $1000, then only benefited, if not benefited.

Then the author says, ” while selecting bond how people select and how we have to select.

How people select bonds:

So they start with a first-lien bond( senior security) and they think, this is very safe and after that, they see the taking risk of the percentage that increases yield.

so this is not the right way

because the first lien, you think it’s safe.

so the author says, ” The right way to select”

The company has to satisfy the minimum standard of safety, after that, we consider which have to choose.

If the lowest seniority (highest yield) bond is not secure and the minimum required of safety not satisfy, then you don’t have to see that company bond and issues failing to meet the minimum required should be disqualified.

means don’t buy that company bonds.

so you have to see from the bottom of the bonds hierarchy and overall debt of the company are satisfy the minimum requirement. (How to invest in bonds)

if they do, then you have to see above of bond seniority for additional safety and you have sacarifying yield.

so we have to do like this, not like people way.

so this is all about how to invest in bonds from chapter 7 of the security analysis book