How to Find a high return Stocks

Hello friends, in today's blog, we see How to Find a high return Stocks for investment. so you will understand the basics of investing and how to be rich in…

hello friends, today, article we see the bond real estate from Security analysis book chapter 10, Specific standard for bond Investment ( continued). In this chapter, we see Criteria 6: Relation of the Value of property to the funded debt. so let’s see the bond of real estate.

As discussed soundness of bond investment depends on the oblique corporation to take the core of its depts, rather than the value of the property on which the bond has a lien.

so we say before that if a company fails, then their properties value also decreases.

so New York Statutes Recommend that the properties value is more than the 66.67% of bond issues.

let’s see an example to understand it

if Bond issued $100 million of any company, then properties value is about $167 million dollars.

so the author explains some special cases in that we have to consider the value of properties.

1 ) Equipment Trust Obligations:

These issues issued by the railroad and also called as equipment trust certificate

In this case, we kept some mortgage for this valuation so railroad companies kept the locomotive like the engine of the railway and their parts as a mortage.

this type of investment company kept and then, they issue the debt.

so in this, we have to consider the Value Because, this instrument, that companies kept as a mortgage, and they are movable and they have their sellable price ( value) because any other companies railway use this type of assets.

If company fail, then does affect on that, because we can see this to other company and get the money.

2) Collateral-Trust Obligation:-bond real estate

In this, company issue, the debt and kept as mortgage as a security purpose, that company, buy that security

means, those are investment trusts, that trust company buy the security of other company and kept their security as mortgage and issue the debt for himself.

In this companies portfolio, we know the market value of the company and we can give them loans while considering their value.

3) Real- Estate bond:

In this case, the main criteria is that how much properties value.

The company gives loans, only 66.67% of the Properties value.

so property fair value matters

so let’s see how we get the property fair value from earning power.

For this, the author gives simple examples, how do we give the loan on properties?

Example,

A home cost is about = $10,000

Rental Value is about = $1200

On the rent, you have to pay the Tax and whatever operation cost, you have to pay

so after this by paying tax and operation cost from $1200

your net income is about = $800

5% mortage, you get on that house, up to 60% of the value of properties, i.e. $6000

so 5% of $6000 = $300

so your coverage ratio is = $800 / $300 = 2.67 X

but any industrial plant they want to issue debt by they want from us

for this, we have to keep more coverage ratio, because, on that plant, this much rental value does not get us.

so after these special cases, the author gives the 7 things on Real Estate bond

1 ) Properties value increases, then rental value Increases:

If properties value decreases, then rental value also decreases

if this does not happen, then people directly buy the house instead of staying in rent, because properties value decrease but rental value increases

so Properties value increases, then rental value Increases.

2) Misleading character of Appraisals:

If sometimes, the real-Estate boom comes, then properties prices ( value) Increases.

so you have to consider those values of experienced buyers and lenders instead of the booming price of properties.

That experienced buyer wants to buy on the price, that price we have to consider instead that, we can think that if that much price is on booming time is have, then we can buy this property or not if the answer is no then don’t buy on that price.

or you can ask your friends, that price of booming time and they are comfortable to buy that price.

so let’s understand with examples

e.g. the building making cost is about $1 million and in boom time, their price increases after building full develop up to $1.5 million,

so 50% profit on making time of that building.

so let’s see a third thing or bond real-estate

3) Abnormal rental, used as a basis for Valuation:-bond real estate

let’s understand this thing, from previous examples, so property value increases 50% means, Original value is $ 1 million and in boom time is about $1.5 million

so your properties rental is abnormally high, so you have to correct them and adjust to the downside.

so in this problem is

If you get a high return i.e. 50% increase so people, try to make the building. and more and more building is developed then supply increases then all building prices suddenly goes down,

so abnormal rental, used as a basis for valuation.

4) Debt based on excessive construction cost:

in boom time, the company can issue more debt, in this boom time

because, properties construction cost is higher because, the demand for making houses is increased, so construction suppliers also increase the rate.

suppose, a cost increase of making houses is about $100 million

so now boom time, their cost is about $200 million

so you can give a loan as per the 60% rule, which is about $130 million

while properties value in boom time is $200 million but their actual price is about $100 million

so $100 million is 60% is about $60 million and you give the loan on that properties is about $130 million means your debt given that properties are not safe, and logically they did not come in 60% rule of properties.

Because, when the value of properties comes to their original fair price, then you are already paying more loan than their fair price of whole properties and loan criteria is up to 60% but you give the $130 million means more 113% of properties.

so debt is based on excessive construction costs, you have to consider this.

5) Weakness of specialized buildings:

In this people make the mistake is that the apartment house, office, storehouse, clubs, the church building

so in this people make the mistake is, they don’t differentiate between them but they have different values.

so in this, you have to treat differently because in this we can not dispose of easily while considering same value

or

this value depends on those companies they have it and they become successful, or not depends on their own value.

those are apartment buildings, they do not depend on that company, because this any can use.

for this, you have to ask for the maximum margin of safety

so for this is good that 50% margin of safety on properties on the loan amount,

in this, you have to ask for a 100% margin of safety.

so this is important is that you have to consider the weakness of specialized buildings.

6) Value-Based on initial rental misleading:

At some time, we take the initial rent for valuing properties, but those are new building their rental obviously is more

so instead of that we have to think like that while considering the new building rent instead that we have to consider after this building is old, what are the rent of this building and that rent we have to consider.

and we can approve.

because initial rent is not for the long term.

7) Lack of financial Information:

In real estate financing, the main character is, they sell the bond to the public but, they hold the stocks privately.

so companies issue, the bond, then they forgot about the bond and bondholders.

and they do not offer any financial data to the bondholder.

so this end some exception and some special case

after that author give their own suggestions

or you can see, how much you pay for buying that or any other experience buyer and lender, how much pay for that

If those are company that deals with the hotel, garage

so for this, you have to provide loan when this hotel is running well. if they are new so don’t make the deal

if they have a successful record then only give.

These are the most important things, the large loss probability in unfavorable conditions.

for this point, understanding the author gives the example

In 1933 after conditions going to improve, but those are a financial district of new york, their activity is less and that reason people gets loses and rental rate also decline so location matters most.

In this, the land has another owner and we build the building on that land.

but we pay regular payment to the landowner

so those companies build the building on that land, this land is the first mortage bond for that company.

but this is not actually the first mortage for you because first mortage of ground to the company is not for you and ground rent this company have to pay

interest coverage ratio = ground rent + interest expenses of the building increases the cost

so this is all bout the bond real estate and also chapter 10 of the security analysis book.

Hello friends, in today’s article we see the classification of securities from chapter 5 of the Security Analysis book. In this chapter, the author explains how people classify securities and how they wrong and the author gives the specific reason and accurate classification.

In this, the author gives the how the grouping of securities is mention by people

let’s see

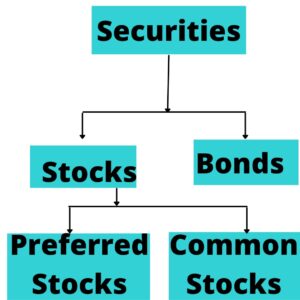

So these securities grouped in two parts i.e. Bond and Stocks

In stocks contain two stocks one is preferred stocks and the other are common stocks.

So we all know those are bonds and the bondholder has the first claim on the company.

If they don’t get the interest on that bond then they have the first claim on the company Asset.

But those are stocks holders they assume that whatever the profits go on that basis they get the maximum profits on shares. (Classification of Securities)

If the shares go down or the company files for bankrupt then they lose the all money because those are bondholders who take the first claim on the company asset.

So the author says, this conventional grouping of securities is not in the right way.

So for the above conventional groups, the author gives the three objections.

Because Preferred stocks get the fixed income, so they one side they are a technical legal partner of a company but actually, they are like bondholder, then that type of results they got also.

This means they can not participate in the profits of the company (dividends), which means they get what is fixed, on that preferred stocks, that much amount only get them. (Classification of Securities)

2. Another problem is people compare the Bond with safety, but this is a big mistake.

So you can say, bond as a whole instrument because they have the first claim on company asset.

Safety does not depend on because they are bonds, it depends on this the comapanies asset that defeats the obligation of the company ( means beat the bond interest payment and other companies problems)

so this point includes the real safety not on this to buy the bond and stay safe is not happen.

Because, if companies don’t have earnings and their asset not capable to pay the bond interest so without that bond is not a safe investment.

3. Title is not used rightly for accuracy purposes, saying anything to any securities just like the following example.

Preferred stocks look like stocks but actually, they work like bond and other deviation also present in financial instrument list like Convertible bond, purchase margin, Warrant, Participant preferred stocks, Non Voting stocks. so this all deviation and also other no voting stocks not we are put in this list that above mentions image, and they put in common stocks but they don’t work like that. (Classification of Securities)

Participant preferred stocks, so these are preferred stocks but we can’t put in preferred stocks, because they are participants.

So the author says, ” this all above classification is not the right way.”

So whatever the characteristics of financial instruments, they are not divided on their characterists.

then the author gives their own Classification.

So they divide them into three classes:

1. Class I (Fixed-value type)

2. Class II (Variable-Value type)

3. Class III ( Common Stock type)

A) Well Protected issues with profit possibilities: in this, the issue is well protected but has profit possibilities.

so that’s why they are variable values, e.g. High-Grade bond, Convertable bond.

B) Inadequately Protected Issues: In this have the profit, but they are not fully protected they have Inadequately protection issues, for example, lower-grade bonds or preferred stocks. (Classification of Securities)

So they have the profits chance because they are very cheap in price.

3. Common Stocks type: In this include share (stocks) that we talk about almost every time.

So now let’s talk about the advantages and disadvantages of these all classes.

so in this difference is those are class II type B have the priority as compare to Class III and they have some protection in class II type B.

Another difference is those are Class II and type B have the profit possibilities, and in this, you get the substantial profit, so but class II type B have the limits so but in Class III in common stocks there is no limit on profits as compare to the class II type B.

So other says, ” those securities that have the characteristics of the common stock, they include in class three, whatever they name are, whatever those are like, common stocks or bonds or convertible bonds or any other financial instruments. (Classification of Securities)

lastly, the author says,” Do not classify securities on the basis of the title of the issue, but the practical significance of its specific terms, and status to the owner.”

So this is all about the classification of securities from chapter 5 of the security analysis book.

Hello friends, in today’s article we see the difference between Investment and Speculation from chapter 4 of the security analysis book. so let’s see the Benjamin Graham point of view.

The Previous Chapter 3: Sources of Information

Bonds and stocks

so people say, ” Invest in bonds is an investment, and invest in stocks is called speculation.”

Outright purchase and purchase on margin( taking loan and buy security)

Some people say, ” We buy the outright purchases that investment and speculation when you purchase on margin ( means taking borrowed money and buy the stocks).

People say, ” Investment is permanent holdings and Speculation is for a quick return.”

other people say, ” Investment is for income and speculation is for profits”

Investment is in safe securities and speculation in risky issues. (Difference between Investment and Speculation)

so authors say, ” this all is bullshit whatever above peoples think.”

So Author starts with the first point and say,

” If you buy bonds that secure but companies earning is not sufficient, so those interest payment not fully paid by the companies, so this is also the speculation.”

so go on to the second point from the above table i.e. Outright Purchases and purchases on Margin

If you want to purchase security and this security is shit, so then this is not a good opportunity so whatever you buy on outright purchases, this also speculation.

or

If you get the wonderful stocks and you get the maximum discount and margin of safety but you buy on purchase on margin this is also Investment and this maybe becomes a good investment.

Temporary and permanent points

This is only the intention of purchase so If someone says, ” I buy this security and keep it so what is the benefit of that if they keep that security. so you have a purpose in buying that whatever your purpose i.e. Profits or income.

So in this, not any temporary or permanent, If they reach at purpose in a short time or long term time, this doesn’t matter, the matter is that purpose is accomplished, whatever the time frame.

Income and Profits

Suppose you get the return whatever is 10, 20%

from where it comes, it doesn’t matter

they come in form of income or profits this all depends on your fundamental circumstance, which means you need every month money for maintaining your lifestyle or you need profits for long terms.

So we can’t say, ” income is investment and speculation is profits”

because of the above fundamental circumstances. (Difference between Investment and Speculation)

Safety and risky point

so safety and risky is dependent on the different points of view of people.

So if one man puts money on a racehorse and he thinks they will win the racing then in his point of view they think it’s a good investment and safe money.

so some people think in 1929, investors think to put money stocks is a safe investment and they think this stock has never gone down because now a new era is beginning and the stock goes high.

so whatever they pay the price, they are justifiable for that stocks in 1929.

This depends on the perspective to perspective so we can’t separate the investment and speculation.

So all this statement neglect by the author and they give his own point of view of definition of Investment and Speculation.

Definition of Investment:

An investment operation is one which upon thorough analysis, promises safety of the principle and a satisfactory return.

If operators not meeting these requirements are speculations.

Thorough Analysis means studying the facts while applying standards of safety and value.

Safety of Principles means, Your principles are not going anywhere in normal circumstances.

Like lite situation happen in the market, except the stream events like recession, depression, etc so then there is no safety in this situation on investment principle, this told by the Benjamin Graham

Satisfactory Returns may be in any form like capital appreciation, dividends returns, or interest payments.

Lastly, investment operation called an investment instead of securities operation as investment operation.

Because any type of securities is an investment or any type of security is speculation. so this only depends on how much price you pay. (Difference between Investment and Speculation)

the author also define another form of Investment

An investment operation is one that can be justified on both qualitative and quantitative grounds.

after this author gives Examples of Speculation.

In Dec 1934, General Electrics stocks were sold at 12 3/4 dollar and paid 6% on $10 pay.

It has one difficulty was they are callable on any dividend date at $11.

So the author says, ” Buying these preferred stocks at 12 3/4 is speculating and we put the 10% of our principal.

so how this happen explain below

Suppose if the issue is called on the very first date i.e. 15 April 1935, then you will get the $11 as call price plus a Dividend.

so how much dividends? for this

Annual dividend = 6% of $10 = $0.6

so for 4 month dividend = 0.6/3 = 0.2.

so, you will get $11 as call price and dividend is 0.2 means $11.02 which could result in a loss of 12%.

so now you think, this is a very simple calculation, so who do like this stupidity.

so, guys, everyone wants to become rich in the stock market and no one wants to do work for that that why we all do stupid things.

So the author says, ” buying these preferred stocks, you are doing speculations.”

You were wagering that issue would not be called for some years to come, therefore it is speculation.

so the author gives the Example of Investment:

In real-time, the same stocks of General Electrics, the issue was called that every month at $11 per share on 15 April 1935. so from this announcement. (Difference between Investment and Speculation)

The price promptly decreased to $11 so the author says, ” this is the investment opportunity.”

So let’s see how?

Now you have the opportunity for profitable short-term investment on margin investors buying.

Suppose, you buy the $11 stocks at on 15 Jan 1935 and you get the $10 per share borrowed money at 2% per annum interest.

so you buy the 1000 shares.

at $11 so net money = $11,000

On April, 15, 1935, you get the $11 plus dividend = $11,150

so this time you have to call the price and get dividends of $150. ( $0.6 per annum and 3 month dividend is 0.15 multiply by 1000 = $150)

so gross profits = $150

so you invest $11,000 and you get the $11,150, but on this, you have to pay borrowed money whatever their interest rates.

so for 3 month interest rat 2% per annum on $10,000 = $50

your net profits were = $100

so you invest $1000 and you take $10,000 as a loan (borrowed money).

The net profit of $100 on $1000 investment, in 3 months is equivalent to = 10% * 4

= 40% Annual return

so this type of return is very much best for an annual year.

Peoples say, that ” investment depends on the past and speculation is depends on the future.”

So after this example, the author gives the four types of investment

1) Business Investment: Your money put in any business

2) financial Investment: Your money put in any securities like bonds, stocks, etc.

3) sheltered Investment: In this, you buy those securities that have minimum risk and they have the first claim on company asset.

4) Analysis Investment: Analysis investment is that investment operation that going through the analysis and they give the promise statement about principle safety and also adequate returns.

So this is the list of types of investment, so this is not an exotic investment list, and about them not other any investment is not like that. and this put randomly without any relations. (Difference between Investment and Speculation)

1) Intelligent Speculation

2) Unintelligent Speculation

1) Intelligent Speculation: Those are intelligent speculation, you only get those risks, you are justifiable on that because you do good studies and whatever your prose and cause on your decision.

So this called Intelligent Speculation

2) Unintelligent Speculation:

In this, you take the risk, without reading that situation you just doing this, because you think these stocks going high.

Because you listen this is a popular company and lots of people talk about this company so this is all are bullshit.

Those are stocks price, and you are paying for that stocks, so we can divide them into two components.

e.g. In 1939, General Electric stocks $38

so analyst judgement says that the investment of that stocks price is $25.

and other remains $13 is that speculation price.

so they represent the stocks market appraisal and long term prospects may be good and peoples bias is that this company is very good and they include the other factor of specular component.

So any investor/buyers pay more than the $25, then they have to recognise, they are paying for speculative possible so the author doesn’t say that this is wrong thinking or right thinking.

they have to just recognise that they are paying for speculation price also and they have to remember this fact then only your mind is set

If you think this is justifiable to pay more than the $25 then, this is Bullshit Think.

and your brain is not set for investing.

lastly, the author gives the relationship between intrinsic value, investment value and speculative value

So those are intrinsic value they can include in the speculative value also, but only for Intelligent Speculation.

So Intrinsic value has two components

If stocks price is equal to Intrinsic value and If they have more than then they include the unintelligent Speculation Value.

so this is all about the Difference between Investment and Speculation from the Security analysis book, chapter 4.

Hello friends, in today’s article we see chapter 2 of Benjamin Graham and David dodd book Security Analysis. Chapter 2 is all about the Fundamental Elements in the problem of analysis. Quantitative and qualitative Factors. So let’s see what is the problem of analysis from Benjamin Graham and David Dodd’s book i.e. Security Analysis chapter 2.

In Previous Chapter 1, we talk about the what is the analysis.

Now Imagine, analysts start the work and how they approach the particular problem, and what is that?

There are two objectives of security analysis, this objective has to be answered by the analyst.

1) What securities should be bought for a given Purpose?

Because in this we have to focus on what we need, and what is your purpose and also what result you expect on that basis you can buy the securities.

2) Should the issue of Security Be bought, Sold, or retained?

To find these two objectives, we have to consider four factors.

1) The Security

2) The Price

3) The Time

4) The Person

In account taking the above four-factor, we can rephrase the second objective just like

A particular Individual at Particular Security can buy, sell or Hold for a particular price and a Particular time.

So let’s go reverse the Sequence of Four factors to make security analysis simple.

I) The Person:-

The person to person what they want, like they want tax assumption upon that they can buy Security.

For Tax assumption, they can buy the Low yield Securities. (Benjamin Graham Security Analysis: Chapter 2)

Or If they can pay Tax, then they can be the High yield Securities.

So this determines the needs of that person’s decision on securities and your decision also depends on time.

So the question that comes to your mind is how on time, so let’s see

How on time, In 1931, the Average return on bonds was 4.3% and, the railroad companies’ high-grade bonds give the 5% yield, so this was an attractive opportunity at that time.

But this same bond becomes Unattractive after 6 months and yield increases up to 5.86% from 4.3%.

When in 1931. the yield of the bond was 4.3% at that time the bond is given 5.2% from the Railroad company. And this was fixed, Whatever the year of maturity of that bond in five years or 10 years.

But in the Market, we get the 5.86% and you get only 5.2%. you get the loss as compared to market rates is 5.86% so this same bond is one time is Attractive and other time is Unattractive.

So your decision also depends on Time.

II) The Price:-

The High-grade bond price was not important when you select high-grade bonds.

Because, their price was rarely high, this happen in 1940 by the author.

So the Most attention was given to this the bond was more Secure or not.

If a bond price was high and then the bond adequately secure then also you have a maximum chance of lose, and also in common stocks have more chance of losing. (Benjamin Graham Security Analysis: Chapter 2)

if you paid the wrong price then you got the loss. This like following quote,

” Buying at wrong price stocks is as much as risky as buying wrong stocks.”

III) The Security:-

The Security and price both are going together.

the Author said, ” Aking this, Which security we have to invest and how much price were we pay for that, Instead that, you have to ask this was what enterprise, we have to invest and in which term we had to invest.”

In terms, not only price come, but they also include, stocks provision of issues and its status issues.

to understand these terms author given two examples,

(1) Commitment On Unattractive Term:-

In this we see, Before 1929, the Urban realistic value constantly increasing for a long time and this investment people think, it was safe, But those terms of issues were disadvantaged able.

Preferred stocks of New York Cities real estate, this provision of issue, was this ranking was junior and unqualified right is not available on dividends payment and status of issues is the New Building was constructing, for that this bond issued for raise money. (Benjamin Graham Security Analysis: Chapter 2)

This was so high-cost construction and there was no reserve for facing a hard time of the company.

Now let’s talk about the price. The price was that the dividend return was 6% and this return was very less than second mortgages but for taking this, there were plenty of advantages

so think these preferred stocks buy or not.

Let’s discuss the second commitment on Attractive terms.

(2) Commitment on Attractive Terms:

In 1932, Brooklyn railroad company sold the 5% yield bonds at $60 and 9.8% Yield of majority.

and the Railway industry is a takeover by the automobile industry.

So unattractive industry was, so let’s see what is the provision

the value of an investment for that this company was raising money, that value is more than that money was raised.

so this company stocks has stable and adequate earning power to pay interest payment and principle and this power is more time than this.

So let’s see the price so this companies bond price was very less than the other companies of subordinate bonds.

But this company price has to be high, generally, those are high-quality bonds, which has high price and yield is minimum, but

In this case, the price is low and the yield is high.

So this company yield was 9.3% and another company yield was 9% and this Brooklyn railroad companies bond also low quality. (Benjamin Graham Security Analysis: Chapter 2)

So author said, ” tell me which security, we have to buy or not”

So from these two examples, the main question was What was more beneficial and profitable.

In the Attractive company buy the security at unattractive terms.

in the unattractive company buy the security at attractive terms.

So the Attractive term was more important than the attractive company (enterprises) and Author also said, ” those were untrained buyers who don’t know how to buy for them, Buy the best and high-quality securities of reputable companies.

Because they don’t know about other things and they don’t have knowledge of other things.

But Those are expert buyers, this people sacrifice some quality because they don’t need that much quality. They buy that much quality for what they need and don’t need more quality.

just like that when you buy a watch, shoes or clothes. If this thing is looking good on you and have adequate quality then why you need the branded and expensive shoes just for looking good and for showing off for this you don’t need maximum quality, and also this is not like that every after the three-day watch is going stop and every time required the watchmaker, then this type of quality doesn’t need. we just need the adequate quality and look goods on us. Same like that those who need the maximum security then they can buy the expensive or high-grade bond of a popular company.

From this, we get the two principles

I) Untrained Security Buyer:

In this those are a weak company or unpopular, then untrained buyer can’t put money in this, because they do, they lose the money. So this is only for the untrained buyer.

II) Security Analysts:

In This point, the author says, ” Nearly every issue might be conceivably cheap in one price range and dear in another.”

So untrained buyers have to stick with that principle, which is the highest quality principle because they have a maximum risk for another place because they don’t have much knowledge of other places. so for those that are popular, that’s awesome good.

But for Analysts, this is not

If analysts think he is right in his judgment, then all world against him, they don’t have to leave that judgment. If their judgment is right, not like an egoist person and says my thinking is right.

Your thinking is wrong and you say, ” this is right so this type of behavior not expect. this like foolishness or stupidity. (Benjamin Graham Security Analysis: Chapter 2)

# Extent of Analysis:

How much we have to do analysis.

In this author says, ” Your practical judgment and your commonsense, how much you have to search deep.”

This author gives the examples

” One bond was that give 3% yield and other was those give 6% yield. So in a 3% yield bond, you have to do less analysis and in a 6% yield bond, you have to see this bond was well secure or not that gives a double return as compared to a 3% bond. so the most probability is that in maximum return the maximum risk in bonds.”

Then Author again says, ” What you do analysis depends on company to company and industry to industry, Like you see five years record of the railroad company and other company like chain store of Walmart. so you see in this company earning for five years, so that ok because this give the reasonable base of Safety.”

But you see oil Producing company and this company is not giving the reasonable bases of safety because this company business depends on external factor like the price of oil when they sell, and how much production in this year or future required this all depends on the external factor.

So they don’t produce maximum they have to produce whatever the demand of oil. If they do more, then the price is fall of that oil. (Benjamin Graham Security Analysis: Chapter 2)

So for this, you have to see which type of industry is also.

so the author says, there are two types of analysis

I) Quantitative Analysis

II) Qualitative Analysis

so let’s see Quantitative Analysis

I) Quantitative Analysis:

In this analysis, you have to see companies statistical data like ( Income statement, Balance sheet, Cashflow, etc)

For this analysis, the author gives the four things about quantitative Analysis

A) Capitalization

B) Earnings and Dividends

C) Assets and Liabilities

D) Operating Statistics

This four-point we see in another chapter because this book is all about the quantitative basis.

so let’s see the qualitative analysis

II) Qualitative Analysis:

In this, the author gives the five things in this analysis

A) Nature of Business

B) Relative position of the company in Industry

C) Geographical and Operating characteristics

D) Character of Management

E) Outlook for company, industry, business in General

so in this chapter, we see some factors of qualitative analysis.

so let’s see one by one

A) Nature of Business:

In this factor, some businesses perform well at some time, and at that same time, some businesses perform badly.

Like that, In 1923-1929, the Generous prosperity time was going on and there is no crash or anything.

Cans manufacture, Cigarette manufacture and chain stores, and also motion picture company, these four company do the well in this period of 1923-1929. (Benjamin Graham Security Analysis: Chapter 2)

But at that same time other companies of the Cotton industry, plumber, paper industry perform badly in this time.

so thinking like that Those companies perform badly at that time and they also perform badly in future also, and those companies perform well in past and also perform well in future, so this thinking is very wrong.

Those companies perform very well or those companies perform very badly in the past so understand that Now time is come to change.

For this, the author gives examples of company

The Public Utility

this company is Unpopular in 1919 when boom happen.

that time, bu tin 1927-1929, this public utility company become speculative

In 1933 the Cotton Industry, which are depressed for a long time, in this time grow very fast.

So you have to see the Nature of the Business factor.

B) Factor of Management:

This factor is double count by the Stock market.

Let’s see how ” those stocks price are earning increases that reflect the stocks, and those companies management is good they also consider in a stocks price.

so this double counting is this for those companies have high earning as compared to the other companies because they are high because they have good management. (Benjamin Graham Security Analysis: Chapter 2)

so management is good than the earning is high and that why we say, stock market double count the Management.

C) Future Earnings Trend:

So in past the earning record is good and increases in past; then this is a good sign but this is not like that in past perform good and they also perform well in future.

So in this what happen in past is fact and what happens in future is pure Assumptions

So we don’t know, what is the trend in the future.

But, we say, in past the average of earning in that may be near in future.

So that much we can say

We can’t say that these are trends that remain the same.

So in this, you are absolutely right or absolutely wrong.

for this author give the two examples

a) In 1929, those railroad companies’ earnings were 5 times more than the interest rate charges for the past 7 years.

So we can make sound judgment in this bond is this investment is good on this bond, but something happen like economic collapse and recession come or any other stream event happens so in this period also company may handle his problem.

In reality, the depression comes after 1929, this company performs well in this situation also.

b) In 1929, the Public Utility company show continuous growth in earnings but fixed charges were so heavy that they consumed nearly all net Income. (Benjamin Graham Security Analysis: Chapter 2)

But people think, This earning also continuous in future. so this prediction goes wrong and they got serious losses.

So people try to quantified the trends, often but it actually is a qualitative factor.

For this, The author says, ” Analysts have to consider future changes, this types of changes happen in future, but from that change, analysts don’t have to do profits from that

Instead of that, they have to guard the future changes

If you try to profits from that changes happen in the future, then you become optimistic, If you think to guard against changes, then you will become more alert.

D) Inherent Stability:

Inherent Stability is like Resistance to the change, which means They can resist the change.

If resist well then stability is good, which means those result in past, we can depend that result may be in future.

But stability is like a trend, People also do with this is quantified it.

but this is also the qualitative factor.

So this qualitative factor is derived by business nature, not a seeing statistical record, this is quantifiable.

So for this, the author gives the examples

E.g In 1932 the preferred stock issues of two companies one is Studebaker( this company sells the motors or manufactures them) and the other is First National Stores ( Grocery company). (Benjamin Graham Security Analysis: Chapter 2)

for previous 8 years

The earnings covered dividends of Studebaker by 26.2 times and that of first National stores by 6.3 times.

So tell me which is better

.

.

.

so obviously Studebaker is good because this company was stable and earnings was 26.6 times than Fixed charges.

But the answer is BiG NO

You are saying by just seeing the data and you quantified them.

Groceries business is more stable because they have stable demand and diversified location and inventory turnover are Rapid.

Those companies that making the Motor, in this has the maximum variation because this depends on popular trends, and also people can buy, in that situation, so we have to adjust as their demand is.

so the company doesn’t have any immunity to those things for this problem.

So many times in quantitative we have to see them from a qualitative point of view to get the proper sense.

and qualitative things, if we try to quantify them and then you don’t have to depend on that

So lastly author says for decision making.

A statistical exhibit is a necessary though by no means a sufficient condition for a favorable decision by the analysts.

So this is all about chapter 2 of benjamin Graham and David Dodd’s book of security analysis.